India now ranks consistently among the world’s top five countries for forex reserves. Yet, past crises have left a lasting impact: building up adequate reserves remains an integral part of RBI policy. Each episode of market volatility has only made the central bank more determined to accumulate reserve assets.

But it has been challenging to build reserves with the same momentum as before. The annual change in foreign exchange reserves has been negative only six times in the past 26 years. Tellingly, three of those occasions occurred in the last four years, including the current one (see chart).

Meanwhile, the Indian rupee continues to weaken, with the RBI walking the tightrope between managing excessive currency volatility while simultaneously accumulating reserves when possible.

Meeting benchmarks

The lessons of 1991 and 2013 have been well learnt. On the one hand, 1991 taught India to hold adequate reserves; sure enough, by end-2025, reserves could pay for 11 months of imports.

On the other hand, the 2013 taper tantrum highlighted a rising dependence on short-term foreign debt. Between March 2012 and March 2013, short-term foreign debt by residual maturity (original short-term debt plus long-term debt maturing in less than a year) shot up from 50% to 59% of total forex reserves. In theory, this meant that if there was no addition to forex reserves, and existing short-term debt was fully repaid, reserves would have reduced by half that year.

No surprise, then, that India was one of the ‘fragile five’ economies that suffered large capital outflows when the taper tantrum unfolded in May 2013. The RBI reacted by shoring up reserves through a special scheme to draw NRI (non-resident Indian) deposits and tightening regulations on short-term external commercial borrowings. The result was a moderation in short-term debt exposure.

How much reserves are enough? When asked this question, former RBI governor Raghuram Rajan reportedly said there was no point at which a country could feel safe, unless it had accumulated trillions of dollars like China. Nevertheless, it is possible to assess reserve adequacy using three standard metrics in the International Monetary Fund’s assessment of reserve adequacy (ARA) framework.

View Full Image

First, import cover measures the number of months of imports that can be financed by reserves. At 11 months, India is well above the recommended three-month norm for emerging economies. Second, the ratio of reserves to short-term debt measures the extent to which reserves cover short-term debt obligations (also called the Greenspan-Guidotti measure). The benchmark is 100%; the ratio stood at 225% for India using residual short-term debt. Third, the ratio of reserves to broad money, which reflects the potential demand for foreign assets from domestic sources, is above the 20% benchmark. Thus, as far as reserve adequacy goes, India has certainly done well.

Reserve account

However, the pattern of reserve accumulation has changed in recent years. This is a matter of concern, because reserves are used not only for external payments, but also to protect against market volatility. To analyse the shift in reserves accretion, it is useful to understand how forex reserves are derived from the international balance of payments (BoP).

In the BoP framework, transactions between India and the rest of the world are divided into the current account and the capital account. India typically runs a current account deficit (exports minus imports) and a surplus on the capital account (it receives more capital than it sends out).

The difference between the two account balances equals the increase or decrease in reserves. Reserves go up when there are dollar inflows from exports, remittances, foreign investment, overseas loans and NRI deposits. They reduce when dollars flow out due to imports, foreign capital outflows or repayment of overseas loans. In a given period, reserves increase or decrease depending on whether there are net dollar inflows or outflows.

Until 2022, a decline in reserves occurred only in a crisis (global financial crisis, 2008-09) or in periods of high current account deficits (2011-12 and 2018-19). At other times, policy actions were designed to accumulate reserves. If there was a net inflow of foreign capital, the RBI absorbed most of it into reserves to prevent excessive rupee appreciation. When there was a net outflow, the RBI sold dollars from its reserves to prevent a sharp fall in the rupee.

Until 2022, a decline in reserves occurred only in a crisis (global financial crisis, 2008-09) or in periods of high current account deficits (2011-12 and 2018-19).

In other words, reserves grew when foreign capital inflows were strong, and declined when there were large capital outflows. Between 2014-15 and 2023-24, annual net foreign capital flows ranged from $20 billion to $80 billion—usually enough to cover the current account deficit. Within the capital account, foreign direct investment (FDI) held steady, averaging about $30 billion annually, while foreign portfolio investment (FPI) was far more volatile.

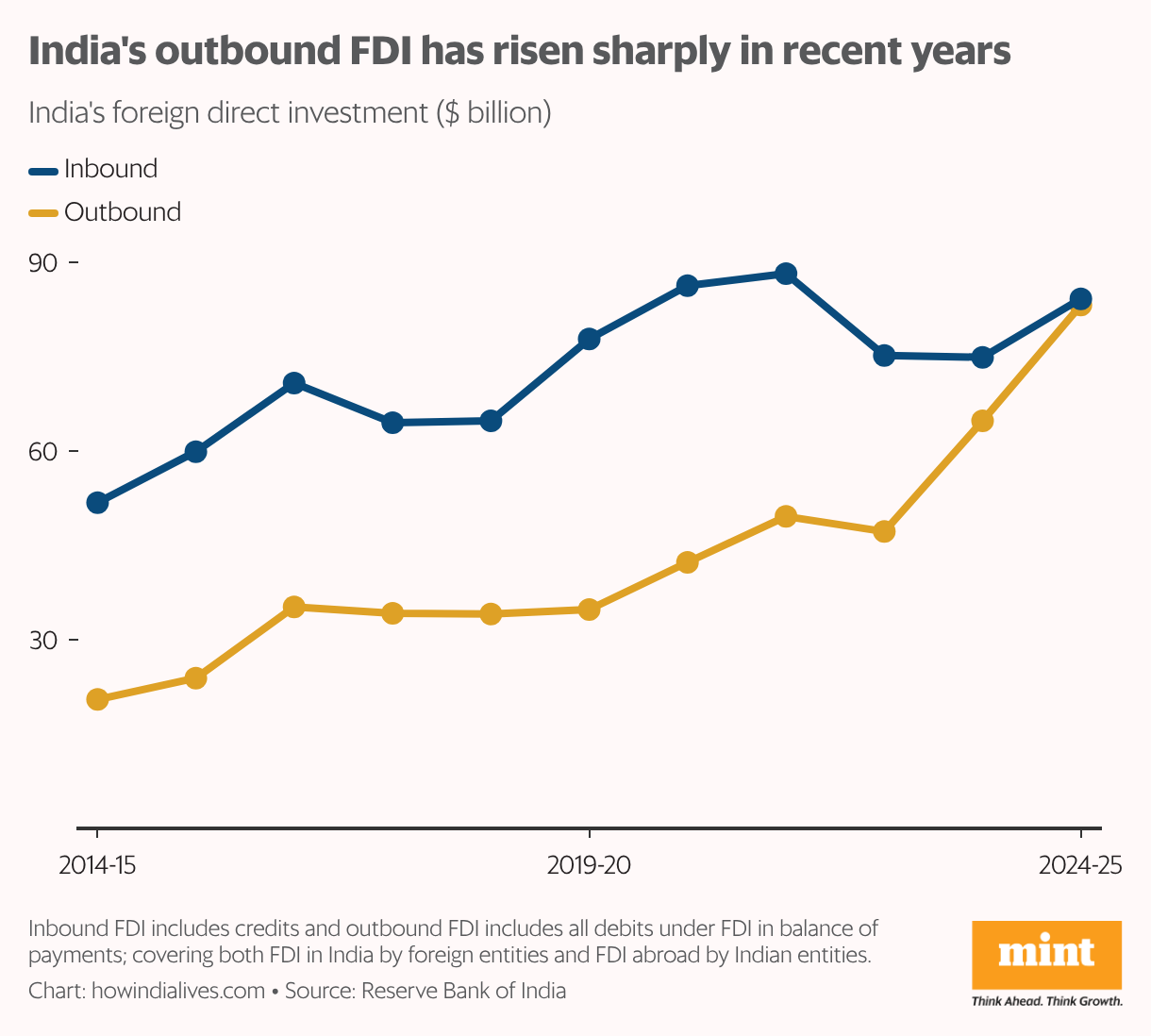

This pattern was disrupted after the pandemic: forex reserves declined by $9 billion in 2022-23, $5 billion in 2024-25 and $10 billion in the second quarter of 2025-26. An analysis of BoP data suggests two explanations. One, a sharp rise in repatriation of FDI in India in recent years: the amount repatriated jumped from around $18 billion pre-pandemic to $44 billion and $ 51 billion in 2023-24 and 2024-25, respectively. At the same time, gross inflows of FDI in India remained relatively stable. As a result, the difference of the two—net FDI—in India has plummeted.

Two, outward FDI by Indian entities has grown rapidly. Net FDI by India was $13 billion in 2019-20, it had more than doubled to $28 billion in 2024-25 (see chart). RBI reports indicate that most of the outward bound FDI by India went to tax havens such as Singapore, Mauritius and the UAE. Media reports suggest that corporates, high-net worth individuals and family offices are exiting India in favour of destinations with stable regulations and favourable investment environment.

Capital flight

The unprecedented events of 2025 have shown that foreign capital inflows, a key source of reserve accretion, cannot be taken for granted. FPI flows were always considered as ‘hot money’, but the rise in outward bound FDI is a new and worrying phenomenon. It is a sobering reminder that our reserves were not ‘earned’ through a trade surplus; rather, they were lent to us by foreigners who can take it back at will.

Contrast this with China, Japan or the Asian tigers, who built most of their reserves from export revenue. How reserves are built matters, especially in today’s challenging international environment. Dependence on foreign capital flows makes India vulnerable to market sentiment. When foreign investors sell off domestic shares or exit Indian ventures, it puts downward pressure on the rupee. If the RBI intervenes in response, reserves are reduced to that extent. The more reserves are drawn down to stabilize the rupee, the more sentiment worsens, and the greater the capital outflow. This sets up a vicious cycle with the potential to destabilize markets.

Given external uncertainties, it is time to take a proactive approach to build and safeguard reserves. It would be a mistake to assume that reserves will grow organically as they did in the pre-pandemic years. The ideal strategy, of course, is to reduce the trade deficit, thereby cutting dependency on foreign capital. But the current climate of trade uncertainty makes this hard to achieve in the short term.

An alternate, and quicker way to build reserves is to work on the capital account: attract more FDI into India, and retain outbound FDI from India. Both monetary and fiscal policies can contribute to this effort; in other words, both the RBI and the government have a role to play in reversing the drain in net FDI flows.

Targeting capital

The RBI is adopting an investment-friendly stance. It has cut the policy repo rate by 1.25 percentage points, reduced the cash reserve ratio by 1 percentage point, and infused rupee liquidity through rupee-dollar swaps. Monetary easing has lowered the domestic cost of capital. In addition, the RBI has eased norms for external commercial borrowing, thereby enabling access to low-cost funding from overseas. It has approved large deals in the financial sector, which have brought in foreign capital. In a recent interview with NDTV Profit, RBI governor Sanjay Malhotra stated that $15 billion of committed or actual investment came into private financial entities in 2025.

View Full Image

The RBI has also made two shifts in reserve management. One, like other central banks of emerging economies, it has been buying gold to diversify from the US dollar. As on 2 January, gold accounted for 16% of the total value of its reserves, up from 6% in January 2022. During this period, 126 tonnes of gold were added to reserves. A higher share of gold hedges currency volatility, and also leads to valuation gains from rising gold prices.

Two, the extent of RBI intervention in forex markets is much lower than it was in 2024. Between June and December 2024, the RBI sold a net amount of $36 billion to stabilize the rupee—a policy that eroded reserves with no impact on the rupee’s fall. In 2025, the rupee was allowed to depreciate gradually, with periodic intervention aimed at controlling volatility.

The upcoming union budget is a good platform for the government to announce FDI-friendly measures. Removing hurdles to doing business in India is an obvious starting point, for two reasons. First, FDI will hesitate if domestic investors are hesitant, as it tends to follow or complement domestic investment. Second, since most FDI operations aim to serve domestic and export markets, the aim should be to create an attractive investment environment for all investors.

The finance minister has already hinted at the possibility of customs reforms in the budget. Rationalization of customs rules along the lines of the goods and services tax (GST) overhaul would be a game changer. Reducing the number of duty slabs and removing duty inversion would benefit both domestic and foreign businesses. The Confederation of Indian Industry (CII) has long argued for a single-window clearance system for FDI, along with time-bound approvals for large investment projects.

India’s regulatory complexity and bureaucratic red tape is challenging for multinationals used to quick approvals and a stable regulatory environment. The recent Supreme Court judgement making Tiger Global liable for paying capital gains tax retrospectively is the kind of ruling that could make foreign investors wary.

Attracting investment is an ongoing process that continuously adapts to changing conditions, as emerging Asia showed in 2025. Vietnam and Indonesia modified investment rules to make it easier for foreign investors to enter, operate, and access local markets. China introduced a new customs system in December: duty-free foreign inputs can enter Hainan province and then be sold domestically with at least 30% value addition. This keeps foreign capital flowing in, boosts activity in relatively-poorer Hainan, and increases domestic consumption. Such innovative ideas are needed to compete for global capital.

Thirty years ago, it was critical to build reserves to protect against BoP disturbances. Today, having accumulated substantial reserves, India can afford to focus on sources of reserve accretion. Instead of viewing reserves as the passive outcome of transactions in the current and capital account, policy should proactively target foreign inflows that are stable and sustainable.

howindialives.com is a search engine for public data