Malhotra responded with what can be described as two insurance rate cuts—50 basis points in June and 25bps in December—to stay ahead of the curve and to optimize the “rare goldilocks” period of low inflation and high growth. A basis point is one‑hundredth of a percentage point.

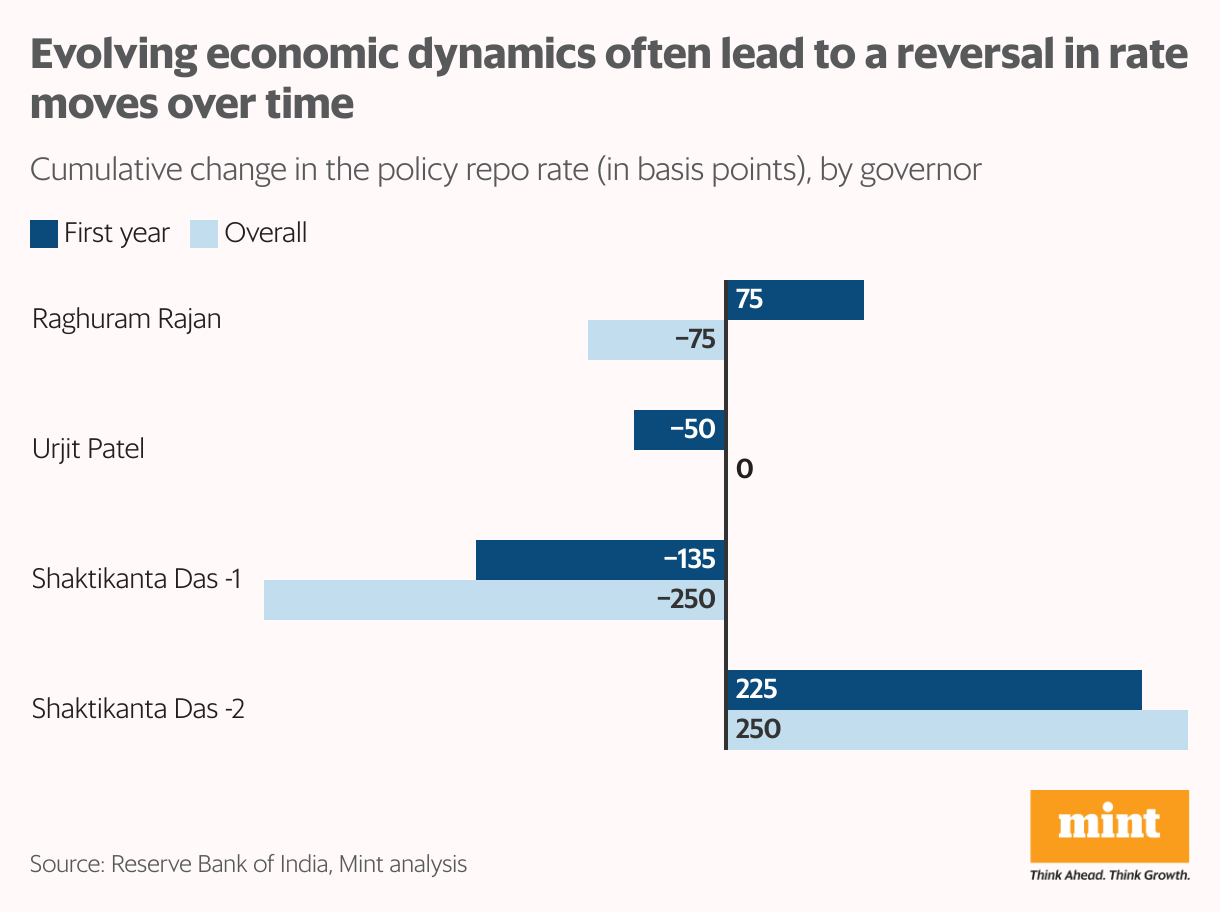

He ended his first year in office with a cumulative rate cut of 125bps, almost as aggressively as his predecessor, Shaktikanta Das, who slashed rates by 135bps in his maiden year (December 2018-December 2019).

Both Das and Malhotra were career bureaucrats who had previously worked in the finance ministry before taking the reins of the central bank. Despite these similarities, Das and Malhotra delivered these cuts against different economic backdrops. Das cut the output gap deemed negative at the time, while inflation was range-bound. Malhotra cut as a precipitous decline in inflation opened a window for lower rates.

On the rupee, Malhotra has diverged from his predecessor, adopting a largely hands-off approach and allowing the currency to weaken.

Experts believe Malhotra is continuing Das’s style of clear communication, but he also has a “give it all” policy. “He believes that when he has clarity, he should just go ahead and give it all, so that the transmission is quicker, instead of doing the step function (like Das),” said Madhavi Arora, chief economist at Emkay Global.

Taking over from governors who oversaw the transition to the flexible inflation-targeting regime (Raghuram Rajan and Urjit Patel), followed by a successful management of inflation through crises (Das), Malhotra had the room to keep liquidity loose. “The inflation target regime is now better anchored, so accordingly there is a preference to keep liquidity conditions somewhat easier,” said Abhisek Upadhyay, senior economist at ICICI Securities Primary Dealership.

The sweet spot

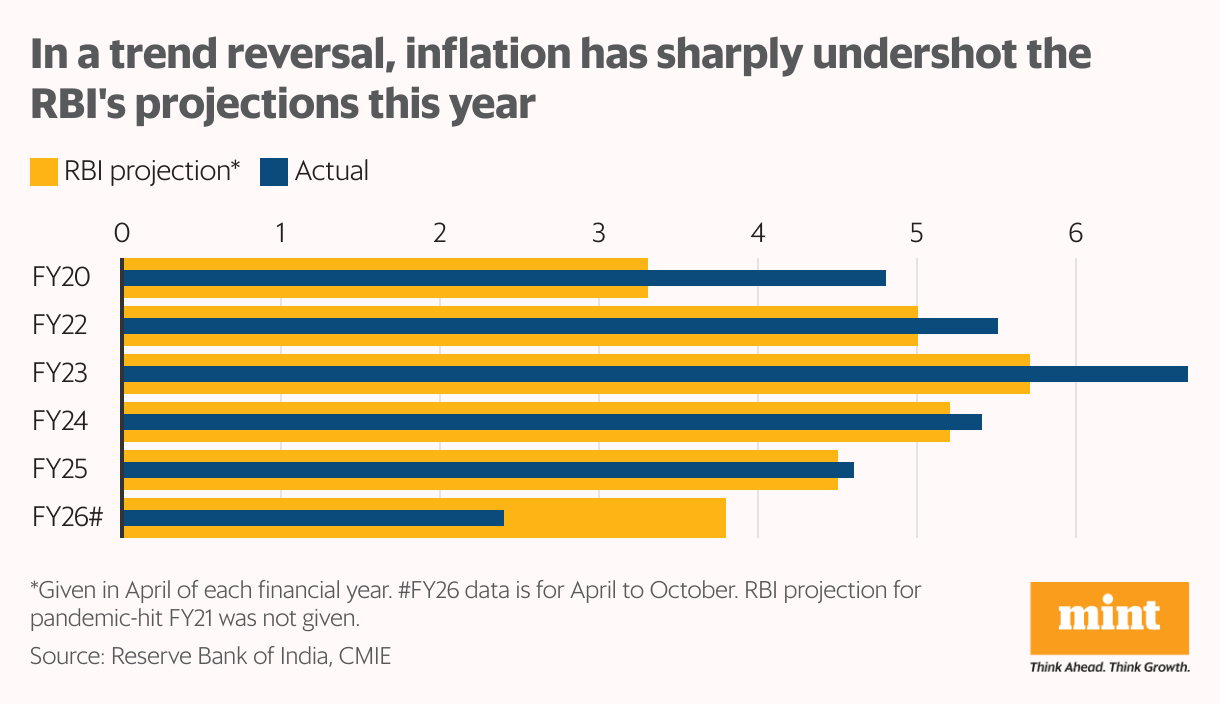

The monetary policy decisions are largely based on one-year-ahead projections of growth and inflation. The RBI consistently underestimated inflation in recent years until this year, when the trend reversed. Inflation not only declined, but also declined so rapidly and continuously that it undershot projections by a large margin, leading to multiple downward revisions in forecasts.

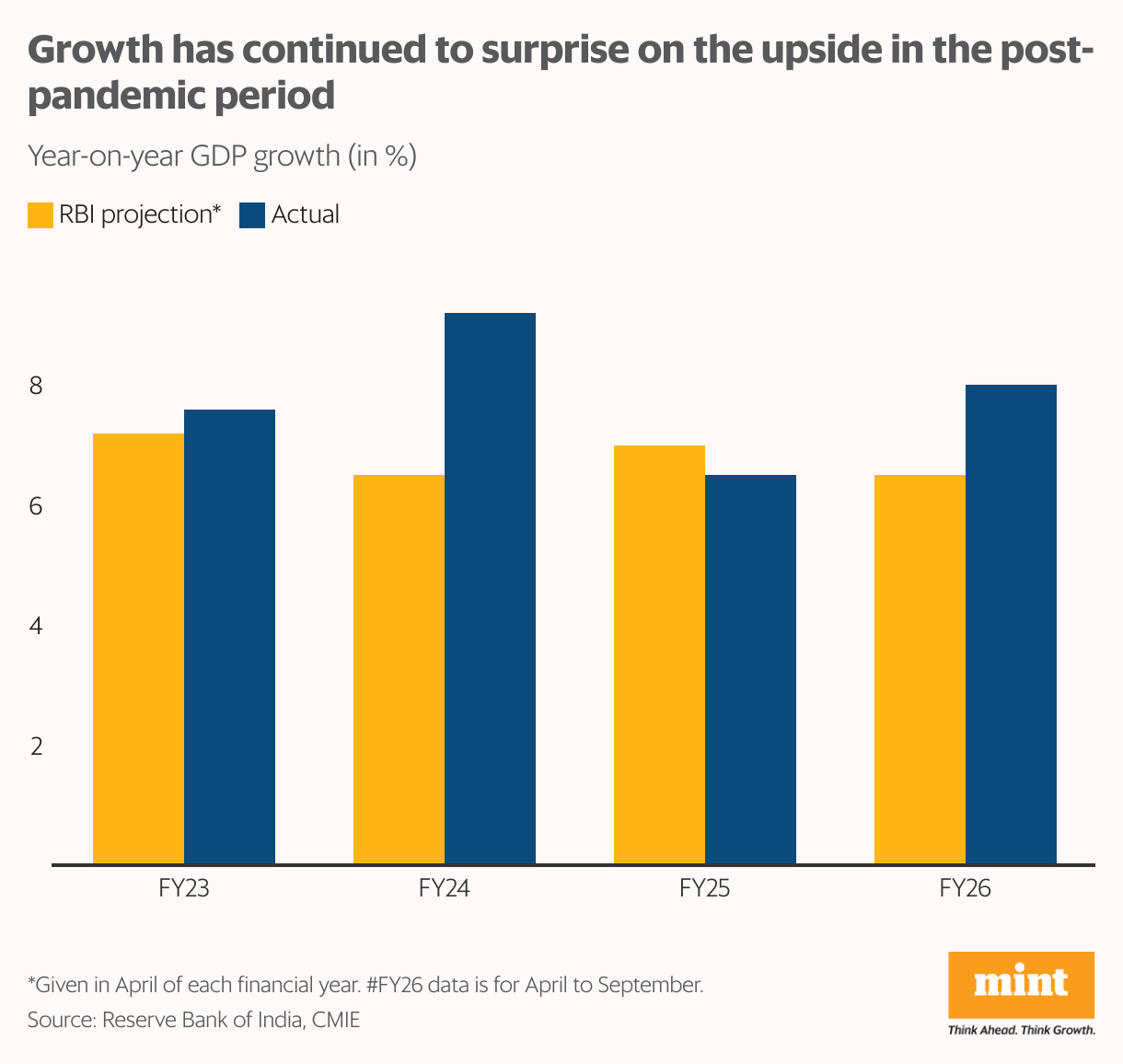

This allowed the space to cut rates. The trend of economic activity overshooting the RBI’s projections continued in the post-pandemic period. This year, it was particularly surprising, as well as relieving, that despite severe tariff-related uncertainty, growth held strong ground in the first half, resulting in an upward revision in full-year growth to 7.3% in the December policy from 6.5% in the April policy.

Reversal on rupee

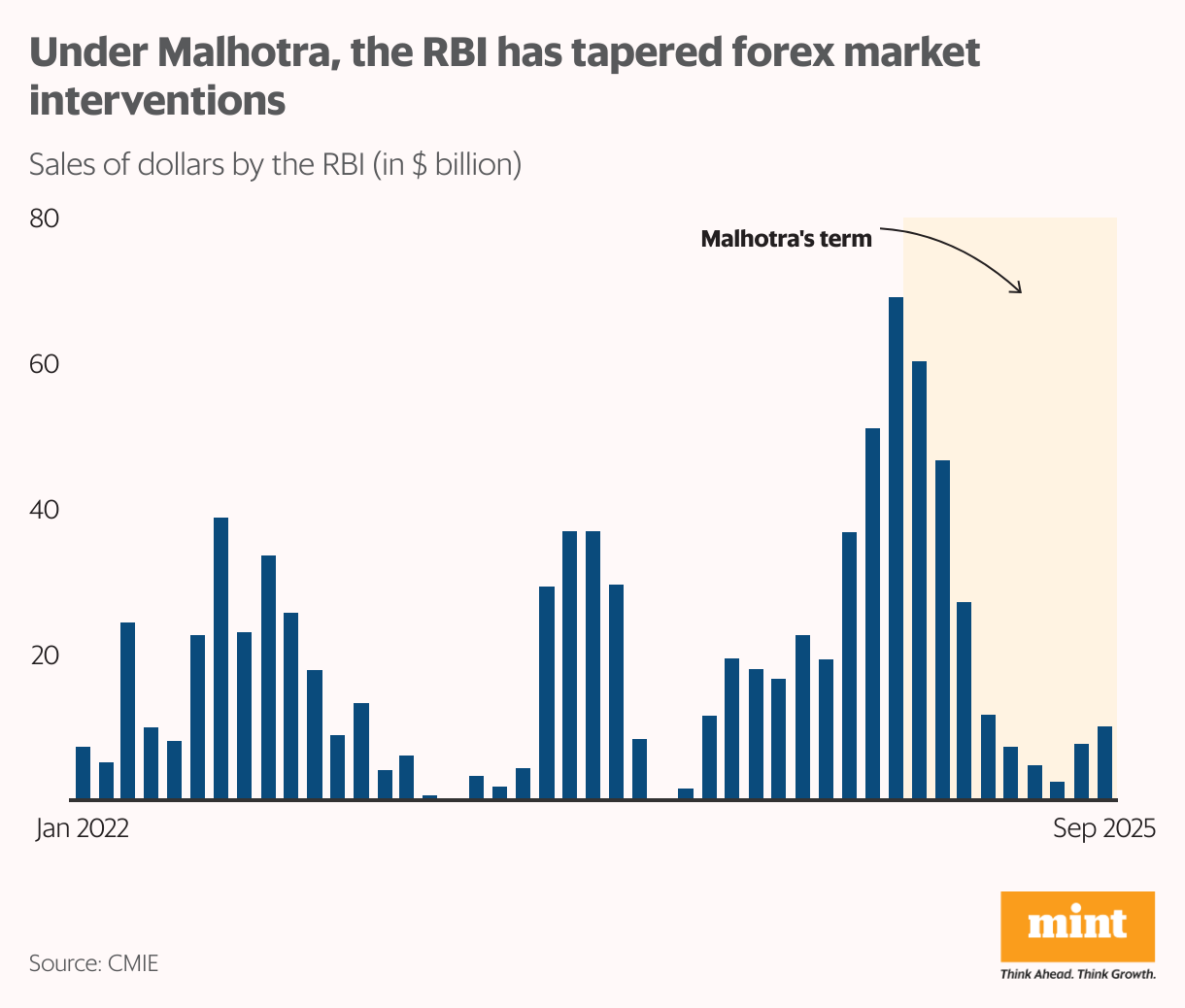

While the inflation-growth dynamic offered a golden opportunity to Malhotra, the weakness in the rupee proved to be a persistent challenge. Even before he took over, the RBI was already facing the “impossible trinity,” which meant the central bank could not simultaneously maintain an independent monetary policy, a stable exchange rate, and free capital flows.

Malhotra hasn’t tried to keep the exchange rate artificially stable. And data bears it out. The RBI buys and sells dollars in the foreign-exchange market primarily to manage the value of the rupee and ensure financial stability in the economy. Towards the end of Das’s tenure, the RBI was purchasing a large amount of dollars to keep the rupee from falling severely. Under Malhotra, the purchases were significantly tapered, even more so in the current fiscal year.

“The current governor has been amenable to allowing the markets to find their own level,” said Upadhyay. “Even as the RBI is there to manage volatility, he broadly has been somewhat more hands-off compared to the earlier regime.”

This shift even earned a reclassification of the country’s foreign exchange regime by the International Monetary Fund (IMF) in November. The multilateral body changed the classification to “crawl-like arrangement” (allowing depreciation but reducing volatility) from “stabilized” (high intervention).

What lies ahead?

Malhotra has so far earned praise for his deft management of a rather normal year despite the global uncertainties, his position on the rupee, and his tilt towards easier liquidity. The first year, though, isn’t an indication of how the entire tenure will shape up.

Evolving economic situations often lead to reversals too, staying true to how Rajan once described RBI governors, “We are neither hawks, nor doves. We are actually owls.” Rajan’s first year was marked by rate hikes as inflation remained high, but his three-year tenure ended with a lower rate. Patel cut in his first year, but his second year marked a reversal. Das continued to ease rates after his first year as the pandemic hit, but it was entirely reversed in his second term as inflation proved stubborn.

Experts said Malhotra moved quickly as he wanted to make the best out of the favourable inflation-growth dynamics. Should this change, so will the monetary policy.