From 2026-27, the government will track government debt instead of fiscal deficit as its primary fiscal target. The new standards require the fiscal deficit to be managed in such a way that the ratio of central government debt to gross domestic product (GDP) declines to 50% (+ or -1%) by 31 March 2031.

This shift is radical in two ways. One, removing the fixed annual deficit target increases spending flexibility—thus allowing the government to spend more in a crisis without worrying about violating the fiscal compact. At the same time, fiscal prudence remains intact because the promise to restrain debt automatically checks excessive spending. Second, as the spotlight shifts to debt, investors and rating agencies will focus on the government’s ability to service its debt obligations in a sustainable manner. In other words, there is bound to be greater scrutiny of the revenue side of the budget.

India’s current debt position is not bad, despite blips in 2008-09 and 2009-10 (global financial crisis), and a sharper spike in 2020-21 (covid-19 pandemic). Both central and overall government debt (as % of GDP) have been trending downward since the Fiscal Responsibility and Budget Management (FRBM) Act was enforced in 2004.

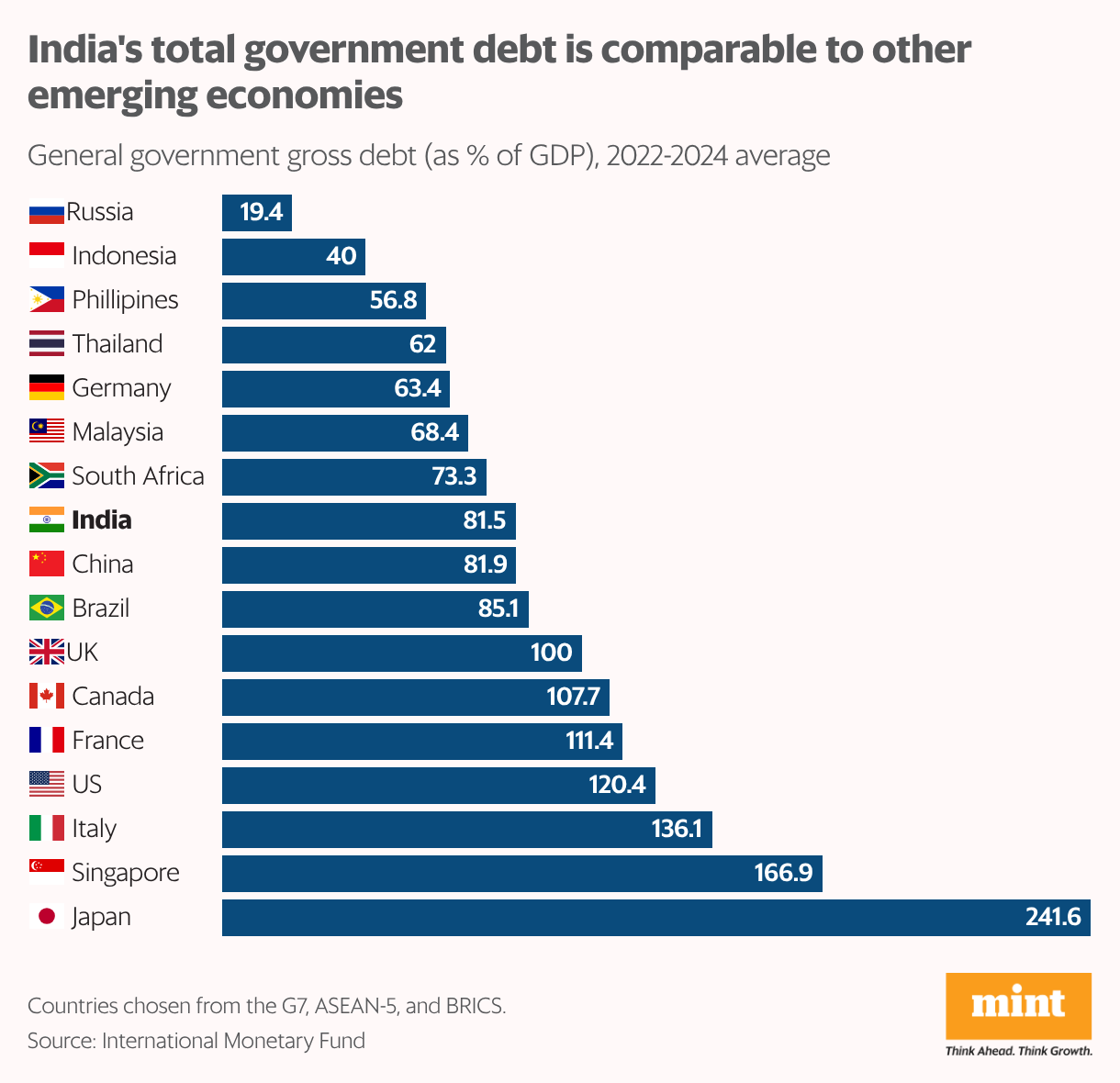

Fiscal discipline has been especially strong since the pandemic spending blitz, resulting in the Centre’s liabilities dropping to just under 57% of GDP in 2024-25, down from 63% in 2020-21. A cross-country comparison is also reassuring: at 81.5% of GDP, India’s general government debt (centre plus states) is comparable to that of other emerging economies, and lower than major advanced economies.

The challenges

A moderate level of indebtedness is a good starting point. However, adopting the debt-to-GDP ratio as a fiscal anchor comes with its own challenges. That’s because markets evaluate debt and deficits in slightly different ways. Debt is assessed based on the revenues available to honour loan obligations; in the case of sovereign debt, these are primarily tax revenues.

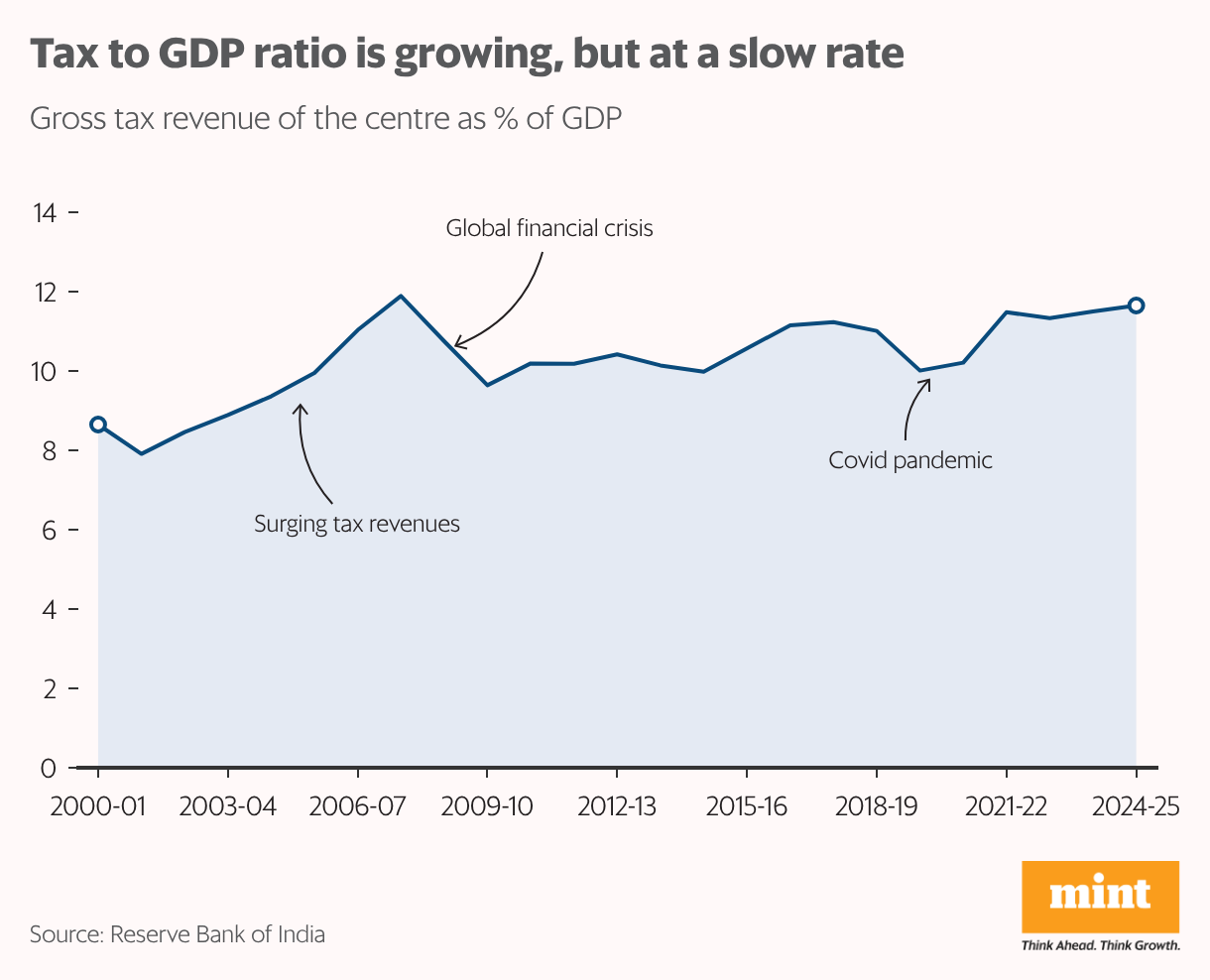

The higher the revenues collected from taxes, the greater the borrowing capacity. For example, the general government debt-to-GDP ratio for G7 economies was a whopping 124%, but these economies also generated tax revenues to the tune of 30-44% of GDP (except the US, with a tax-to-GDP ratio of 26%). In contrast, India has a lower debt ratio, and most of its debt is domestic, but tax revenues form merely 11.9% of GDP.

The reasons for our narrow direct tax base are well known: low-income levels, a high share of the informal sector, and exemption of agricultural income from tax. Indirect taxes such as goods and services tax (GST), which are universally levied, contribute to about 42% of the total tax revenue collected by the Centre.

The World Bank research shows that the relationship between tax revenue and economic growth is positive but not linear: countries jump into a higher income category at specific thresholds of tax-GDP ratio. For instance, the transition from low-income to middle-income country is likely to occur at a median tax-to-GDP ratio of 13%, and is typically preceded by a decade of 3-4% growth in the ratio.

The rationale is that higher tax revenues boost development by enabling higher public spending on health, education, social welfare, and physical infrastructure. India experienced a similar transition in the 2000s. Surging corporate and personal income tax revenues raised central tax revenues by over 3% between 2000-01 and 2007-08, resulting in the country’s upgrade to middle-income status in 2009. Since then, unfortunately, the tax-to-GDP ratio has stagnated and remains below 12%.

Without higher tax revenue, it will be tough to reduce central government debt by about 1-2% of GDP annually over the next five years, as envisaged by the government’s medium-term fiscal strategy. Efforts to streamline tax collection and payment have been quite successful, but India has far to go before it reaches the 20-30% plus tax-to-GDP ratios observed in high middle-income countries. That’s why the government falls back on non-tax revenue—dividends from public sector undertakings and the Reserve Bank of India (RBI)—to meet the fiscal deficit target.

The sustainability question

This is not sustainable: as we move to a more globally aligned fiscal anchor, the sources of funding debt and deficits will also have to align with accepted practices. The large majority of countries, including India, derive less than one-fifth of government revenue from non-tax sources. To stay within these limits, while maintaining a brisk pace of public spending, will require a steady rise in tax revenue.

The year ahead comes with multiple fiscal pressures. Some states have rolled out freebies despite inadequate revenues; in response, the finance minister publicly warned states against borrowing for such schemes. Though states are not covered under the new fiscal compact, their fiscal discipline is critical, because total government debt is the globally tracked metric.

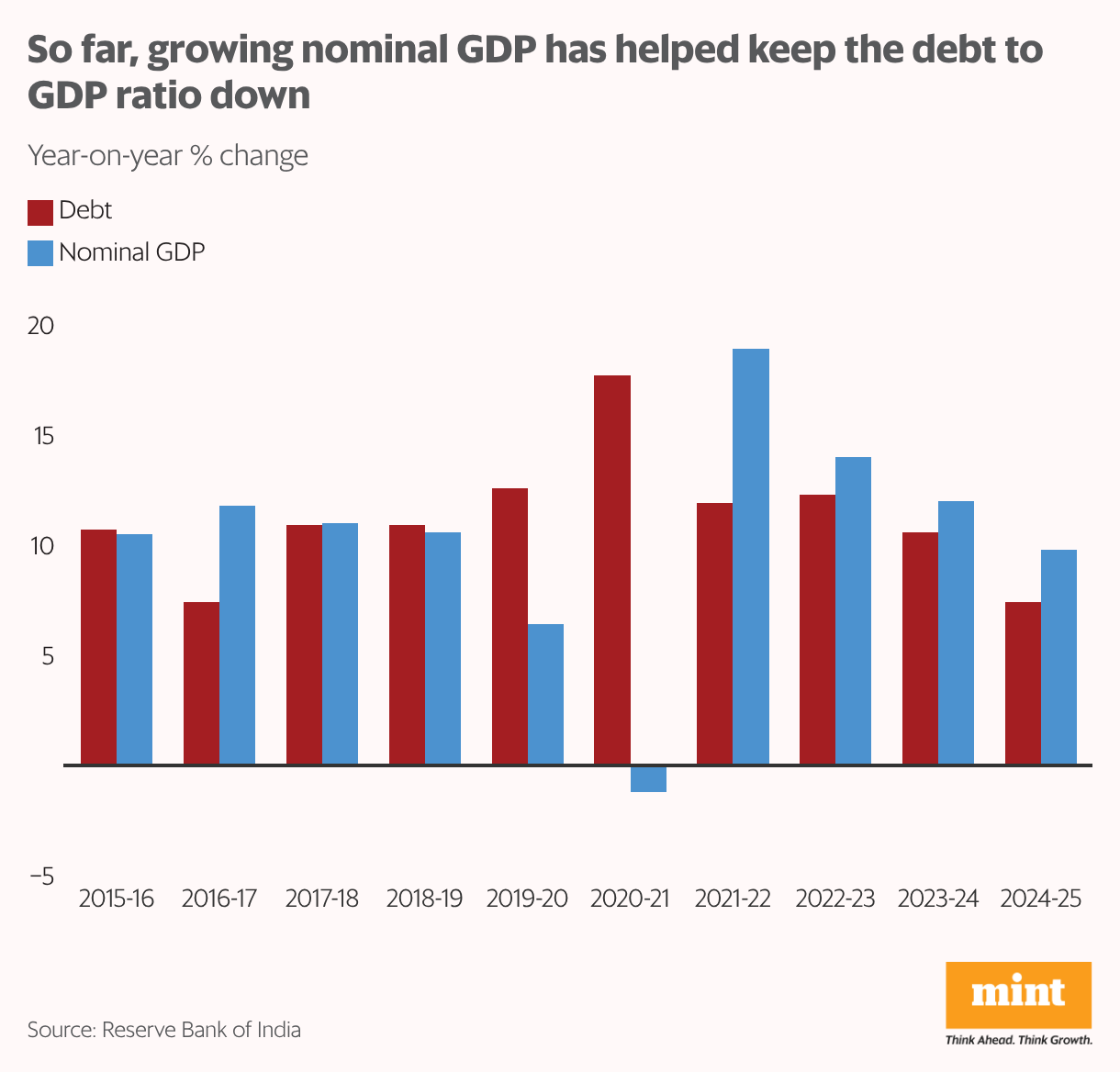

The eighth pay commission report is expected to be tabled in early 2027; the resulting hike in pay and pensions for civil servants is likely to increase government expenditure. On the revenue side, the government is betting that the consumption boost from cuts in income tax and GST rates will make up for foregone tax revenues. All this will have to be managed in a challenging external environment. In the past, fiscal consolidation has been led by growth: a rising nominal GDP reduces the debt-GDP ratio.

Unfortunately, nominal GDP growth is estimated at 8% in 2025-26, and forecast to be around 10-11% next year. The government will have to work on building up revenue if it wants to hold on to its hard-won reputation for fiscal prudence.

The author is an independent writer in economics and finance.