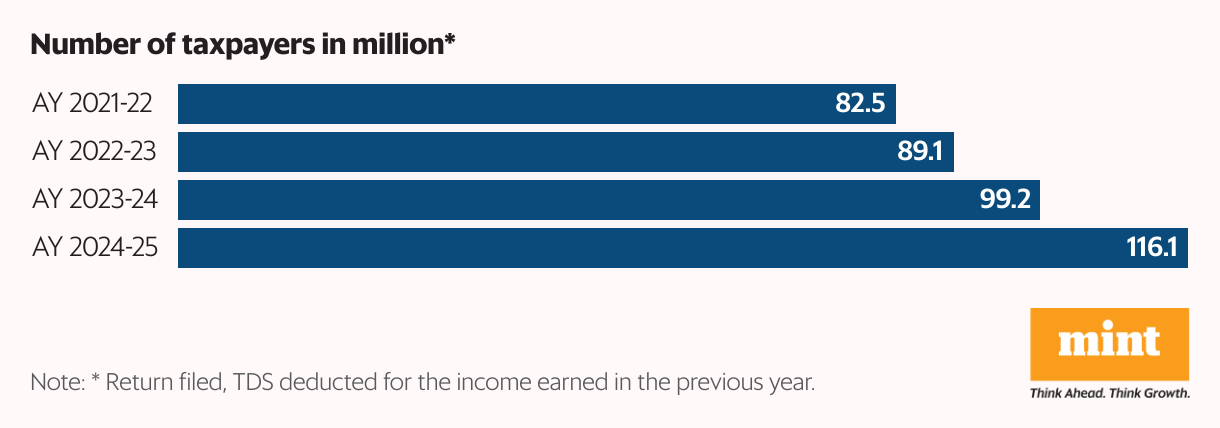

In assessment year 2024-25, covering income earned in FY23-24, the total taxpayer base jumped 17% year-on-year to 116.1 million, while the number of returns filed was at a low 8.08 million, up 5.9% y-o-y, CBDT data released earlier this week showed.

The trend is consistent over the past four years and the gap has widened, CBDT data showed. Total taxpayer base refers to both return filers and those with TDS deducted.

CBDT chairman Ravi Agrawal told the media on 17 November that the tax authority was hopeful of meeting its ₹25.2 trillion direct tax collection target this year and that it was connecting with taxpayers through emails wherever gaps have been noticed.

In FY25, total TDS collection accounted for 35% of the ₹27 trillion gross direct collection, although it is not known what share of TDS collection is from those who did not file returns or their tax liability.

Greater TDS coverage indicates greater oversight of economic activity, which enables the Income Tax department to pre-fill tax returns based on transactions it is aware of, inform tax payers about TDS deducted transactions so that they do not miss out any income while filing returns, and run campaigns by reaching out to assessees for greater voluntary compliance. Return filing is essential for claiming tax refunds.

Experts point to various reasons why the gap is increasing.

Reasons behind the increasing gap

Riaz Thingna, partner at Grant Thornton Bharat LLP, said the trend reflects the government’s success in leveraging digitization and advanced compliance tools. According to Thingna, tax being deducted at source may make some taxpayers feel that their taxes are paid and compliance obligation is over.

Also, non-residents covered by certain provisions in the Income Tax Act are exempt from filing, subject to conditions. Some tax payers who miss the original deadline subsequently file belated returns, explained Thingna.

Amit Maheshwari, tax partner at AKM Global, a tax and consulting firm, said an increasing number of individuals are now being categorised as taxpayers because tax is deducted at source on incomes such as interest, professional and contractual receipts, certain high-value transactions, and even in cases where their overall income does not require them to file an income-tax return.

“The expansion of reporting requirements through annual information statement (AIS) and form 26AS, coupled with enhanced compliance systems and stricter monitoring by the tax administration, has strengthened TDS-driven inclusion,” said Maheshwari. “Consequently, the taxpayer base is growing at a considerably faster pace than the number of actual ITR filers.”

Further, senior citizens who receive dividends or interest income below their taxable income may receive such income post TDS, but they may not file tax returns, explained Samir Kanabar, tax partner at EY India. “Similarly, all individuals below taxable income limits may not be filling tax returns,” he added.

Clubbing of income of different persons in a family can also lead to a situation of taxpayer growth exceeding return filing growth.

“For example, the income of a spouse or children may be clubbed with that of the other spouse or the parent. In that case, while TDS may have happened in the PAN of either of the spouse or child(ren), but single return may file returns,” said Kanabar of EY.

Expanding TDS coverage

The government has been consistently expanding the coverage of TDS on transactions in the economy, some applicable rates of which were reduced in FY25 to improve ease of doing business.

For example, from 1 September 2019, the government introduced a 2% TDS on cash withdrawal exceeding 1 crore in a year from a bank account to discourage the practice of making business payments in cash.

Also, from that date, the government introduced a 5% TDS on payments to a contractor or professional exceeding ₹50 lakh made by individuals and Hindu Undivided Families (HUFs). This has been lowered to 2% from 1 October 2024 as part of the TDS rationalisation effort.

Also, effective from 1 July 2021, there is a 0.1% TDS on purchase transactions above ₹50 lakh in a year if a buyer has more than ₹10 crore annual sales.

Also from 1 October 2020, a 1% TDS on certain payments from e-commerce platforms to platform participants was introduced, which has now been reduced to 0.1% from October last year.

Finance minister Nirmala Sitharaman said in her Union budget speech on 1 February this year that the number of TDS rates were being lowered and the threshold for its applicability being raised in order to benefit small tax payers receiving small payments and for easing difficulties.

“The scope of TDS has been expanded to a large extent. CBDT should analyse the data and find a way to refund the TDS amounts received from individuals with income below the taxable threshold and have not filed tax returns,” said Ved Jain, former president of Institute of Chartered Accountants of India (ICAI).

“Also, in cases where the individuals have a taxable income but have not filed returns, appropriate steps under the law should be taken,” he added.

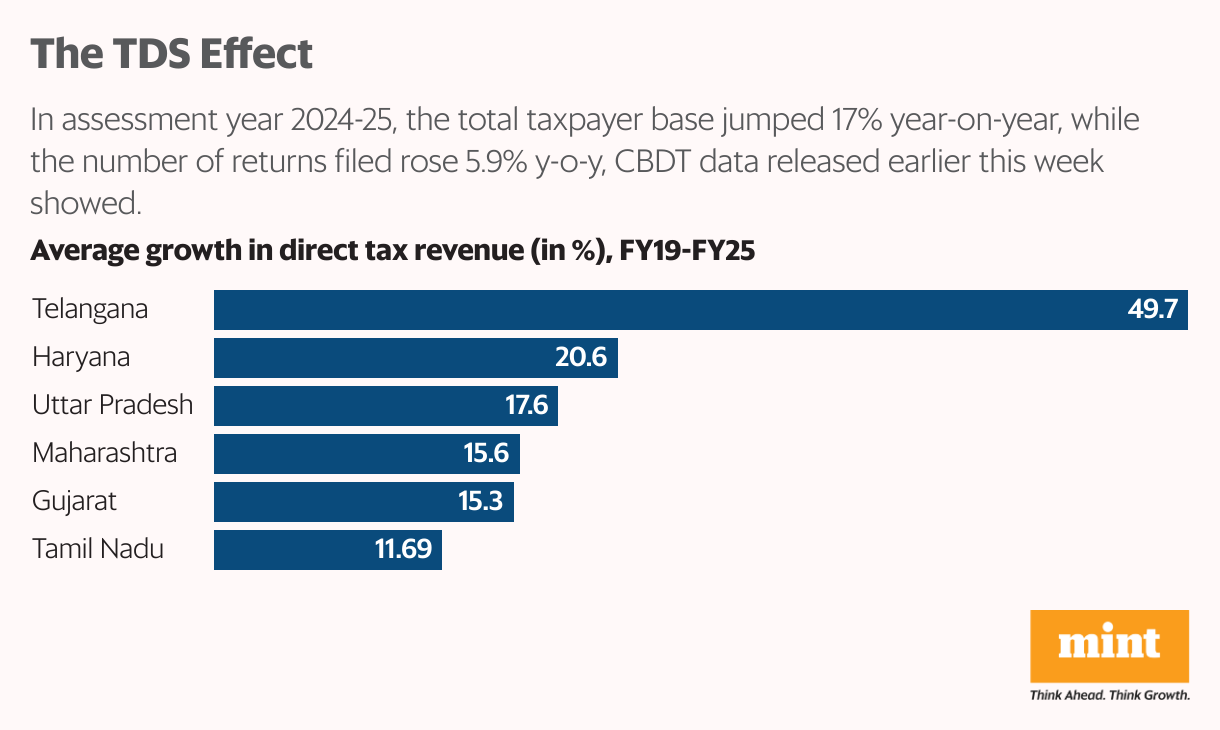

Telangana on top

CBDT data also showed that Telangana has emerged as the fastest growing state in terms of contribution of direct taxes to the exchequer, followed by Haryana and Uttar Pradesh among large state economies.

Between FY19 and FY25, Telangana’s direct tax collection has jumped eight-fold to ₹97,860 crore. In these years, its average direct tax collection growth was a spectacular 49%.

“Telangana’s sharp rise in direct tax contributions is closely linked to Hyderabad’s emergence as a major IT and services hub,” explained Maheshwari of AKM Global. “The city’s rapid expansion has boosted corporate profitability, increased the number of high-income professionals, and significantly enhanced TDS inflows.”

The state’s business-friendly policies and targeted incentives for the IT/ITeS sector have further attracted fresh investments, contributing to a wider and more robust tax base, he added.