Small enterprises continue to rely heavily on informal sources such as friends and moneylenders for small-ticket loans, primarily borrowings below ₹50,000, highlighting persistent gaps in access to formal credit, the Economic Survey tabled in Parliament on Thursday showed.

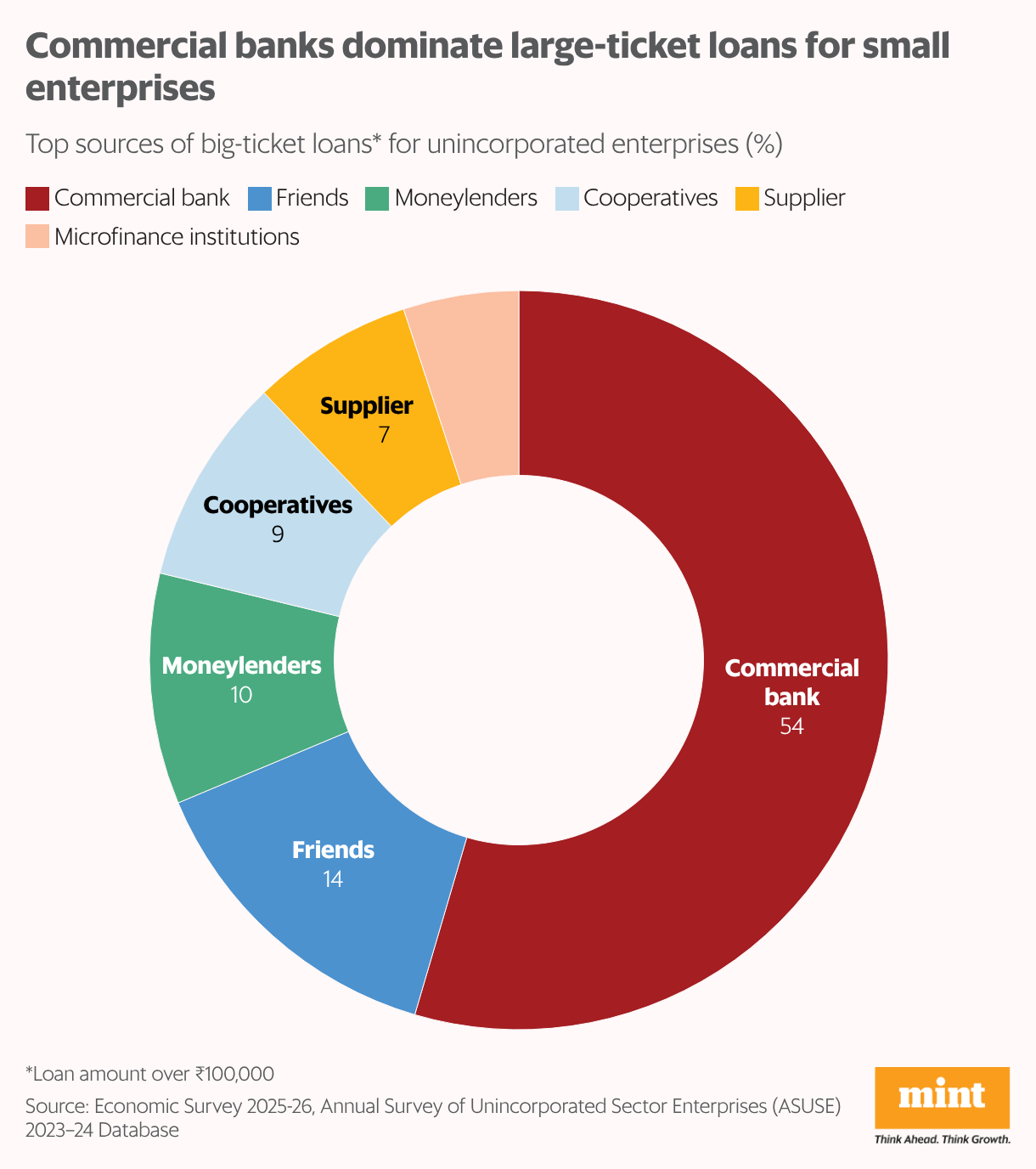

The survey, citing analysis of data from the Annual Survey of Unincorporated Sector Enterprises (ASUSE) 2023-24, points to a sharp divergence in financing patterns by loan size for micro and unincorporated enterprises. Commercial banks are the biggest source of large loans (ticket size above ₹1 lakh), accounting for 54% of outstanding loans.

By contrast, for loans below ₹50,000, friends account for 42% of outstanding credit, followed by suppliers at 23%. Formal institutions such as banks, cooperatives and microfinance institutions together account for just 23% of loans in this segment.

“Friends continue to serve as an important financing source owing to strong personal relationships and the availability of low- or zero-interest loans without collateral, particularly for small and urgent funding needs,” the survey for fiscal year 2025-26 said.

While improved access to formal lenders has helped reduce dependence on informal finance for moderate and large loans, major gaps remain for small-ticket borrowings.

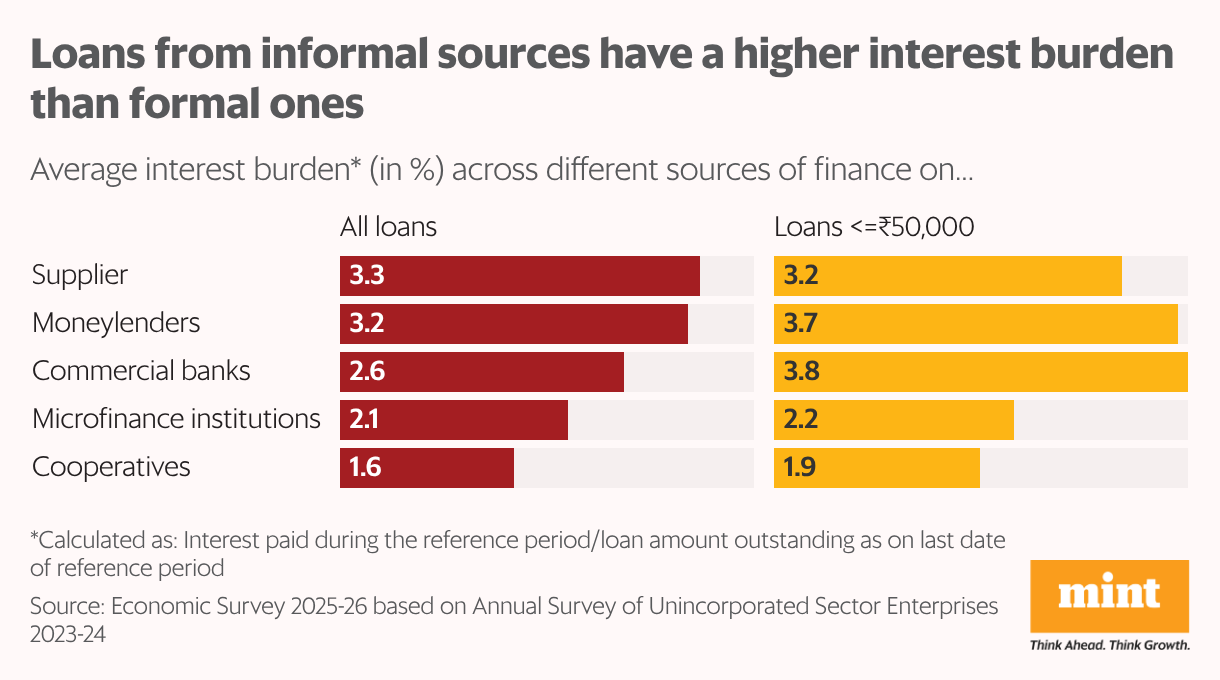

This pattern could come at a cost for small firms in the form of a higher interest burden. The survey’s analysis shows that loans from informal sources typically carry higher interest costs than those from formal banking channels, a trend that extends to small-ticket loans as well. For instance, the average interest burden for loans from moneylenders stood at nearly 4%, compared with just 2% from cooperatives.

Several structural inefficiencies hinder uptake of formal credit in the micro-loan segment. On the demand side, the survey attributes documentation barriers, lack of financial literacy and thin credit histories as primary reasons. For lenders, weak profitability disincentivises greater participation in small-ticket lending.