Wait-and-watch

Four key central banks are scheduled to announce their monetary policy decisions in March, with policymakers widely expected to keep interest rates unchanged amid uneven inflation, mixed growth signals and rising political uncertainty.

Last week, India left the policy repo rate unchanged as growth outlook improved from a potential India-US deal, while inflation is expected to rise above 4% mid-point target by the first quarter (April-June) of FY27.

In the US, the Federal Reserve is likely to extend its pause as inflation remains above the 2% target and economic growth continues to outpace its long-term potential, leaving little room for near-term easing. Leadership uncertainty, including the prospect of Kevin Warsh taking over as Federal Reserve chair later this year and concerns over political interference are also expected to reinforce a cautious stance.

The Bank of England, while moving closer to rate cuts, is expected to hold for now as it weighs cooling demand and easing inflation against still-elevated price pressures and a fragile recovery. In the euro zone, the European Central Bank appears comfortably on hold, with inflation below target but growth proving more resilient than feared and exchange-rate moves largely absorbed into its outlook.

However, Japan stands apart with its central bank expected to maintain its tightening bias, keeping rates steady in March, but signalling further increases later in the year as wage growth firms and a weak yen risk adding to inflationary pressures.

EMs reloaded

Emerging markets are finally breaking their long streak of underperformance. For nearly 20 years, these developing economies grew faster than the West, but their stock markets failed to keep up. That changed in 2025. The MSCI Emerging Markets Index surged by 34%, much higher than the 21% return of the developed MSCI World Index.

This momentum has carried into early 2026, with emerging market shares already up another 9%. Stronger local currencies and higher returns on domestic bonds have added to the momentum. Besides, a weaker US dollar also played a role in lowering the cost of dollar-denominated debt and boosting exports.

Historically, EM stocks have tended to rally when the dollar weakens, suggesting there may be more room to run. In all, emerging markets remain relatively cheap compared with developed markets, and they are more resilient than in the past. Stronger institutions, healthier central banks, and better preparation for economic shocks have made them safer bets.

With the International Monetary Fund (IMF) predicting these economies will continue to outpace the rich world this year, investors now have a compelling reason to look beyond the MSCI World—for growth, diversification, and higher returns.

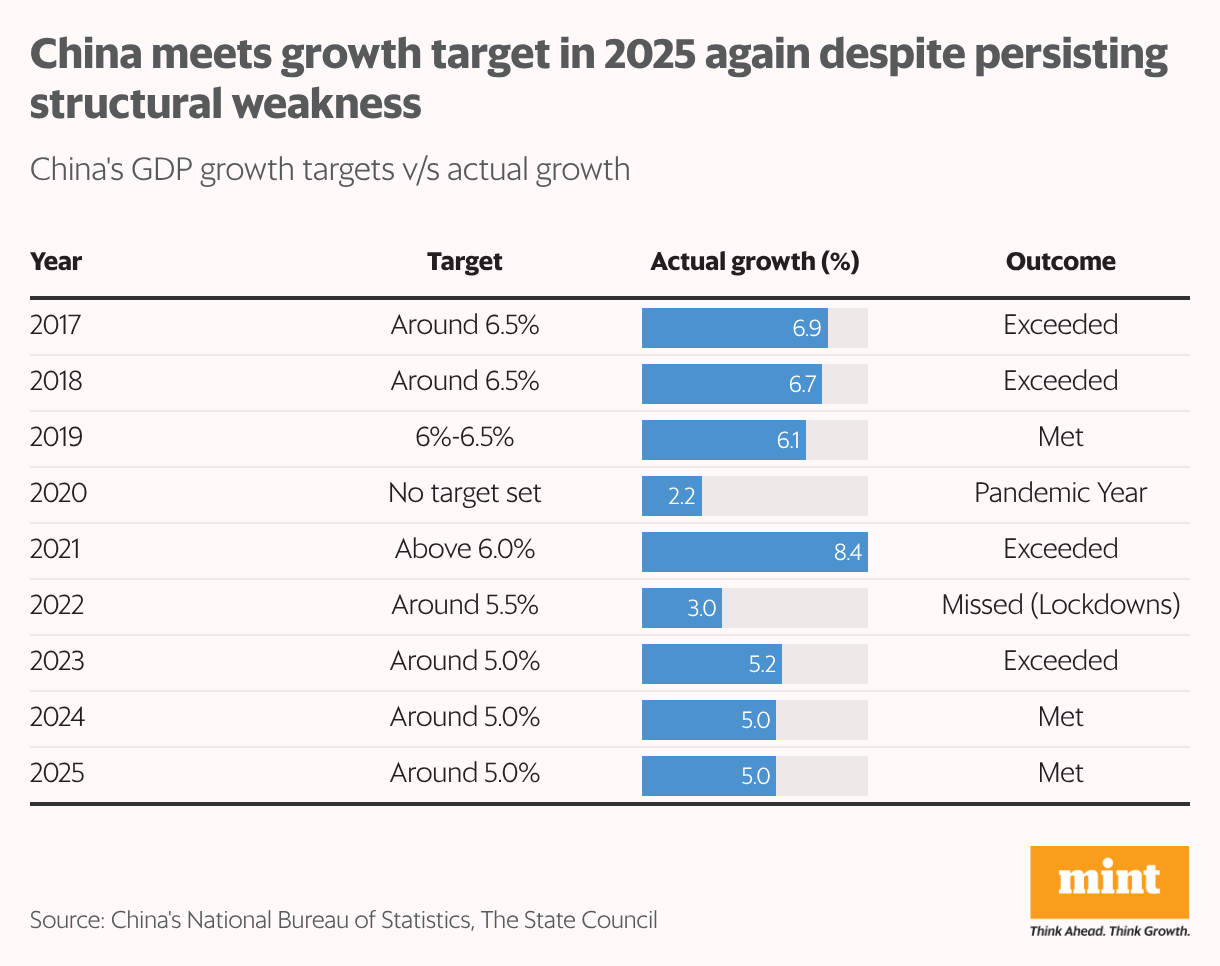

Growth with strains

China hit its 5% growth target again in 2025, but the way it maintained its track record speaks about its strength as well as its weaknesses. Growth was carried overwhelmingly by exports, which surged despite high US tariffs and pushed the trade surplus to an unprecedented $1.2 trillion.

That export engine compensated for a domestic economy that remains stubbornly weak: households saved more, spent cautiously, and showed little confidence, while the property sector continued to drag investment lower.

Beijing’s post-property-crisis strategy has been to channel credit and policy support toward factories rather than consumers, deepening overcapacity and forcing producers to seek demand overseas. This has worked so far, but at a rising cost. Trading partners are growing uneasy as Chinese goods flood their markets, raising the risk of retaliation.

A relatively weak yuan has amplified this effect, even as authorities have recently allowed the currency to strengthen slightly and offered selective trade concessions. Experts believe that without a stronger push to lift household incomes, repair the property sector and boost domestic demand, China risks slower growth at home and sharper resistance abroad, risking its export-heavy model as well.

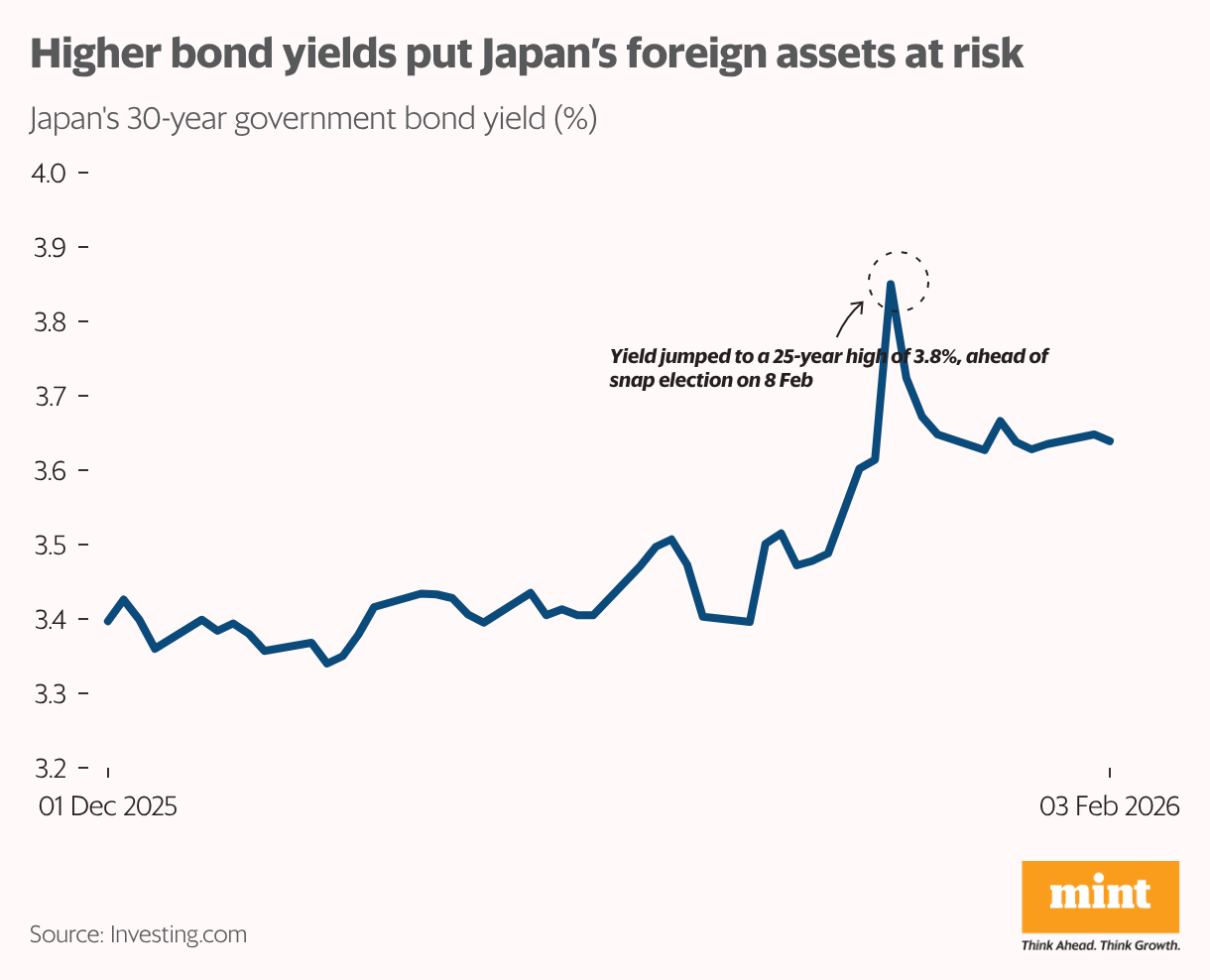

Japan jitters

Japan’s 30-year government bond yield jumped to 3.8% on 20 January, the highest level in 25 years, as investors priced in the risk of a snap election that could lead to more fiscal spending. The spike highlights growing concerns over Japan’s exceptionally high debt-to-GDP ratio, which exceeds 250%, leaving the government more sensitive to changes in interest rates and fiscal policy. High yields make borrowing more expensive and raise questions about the sustainability of Japan’s long-standing fiscal model.

At the same time, Japanese investors remain among the world’s largest holders of overseas assets. According to The Economist, financial institutions in the country hold over $6 trillion in foreign securities. To protect that money from currency swings, they used “hedging,” but that has now become very expensive.

With Japanese yields finally rising, some investors may find it simpler and more profitable to repatriate funds and invest domestically. However, the spike proved temporary, and yields have since eased to around 3.6%, reflecting a market recalibration rather than a broader panic.