Chief economic adviser V. Anantha Nageswaran recently pointed to the remarkable decline in inflation in recent months and suggested that India may even be witnessing a structural transformation in inflation.

Certainly, inflation data for this year support this idea. The retail inflation rate has dropped from 4.3% in January to 0.25% in October; wholesale inflation is down from 2.3% to (-)1.21%.

For an inflation-prone country like India, low inflation rates for a sustained period are an achievement in itself, and the Reserve Bank of India (RBI) has rightly been praised for its deft management of the situation.

But if, indeed, the Indian economy is moving towards structurally lower inflation, there are some other macroeconomic variables that could face a significant impact.

Inflation-rupee link

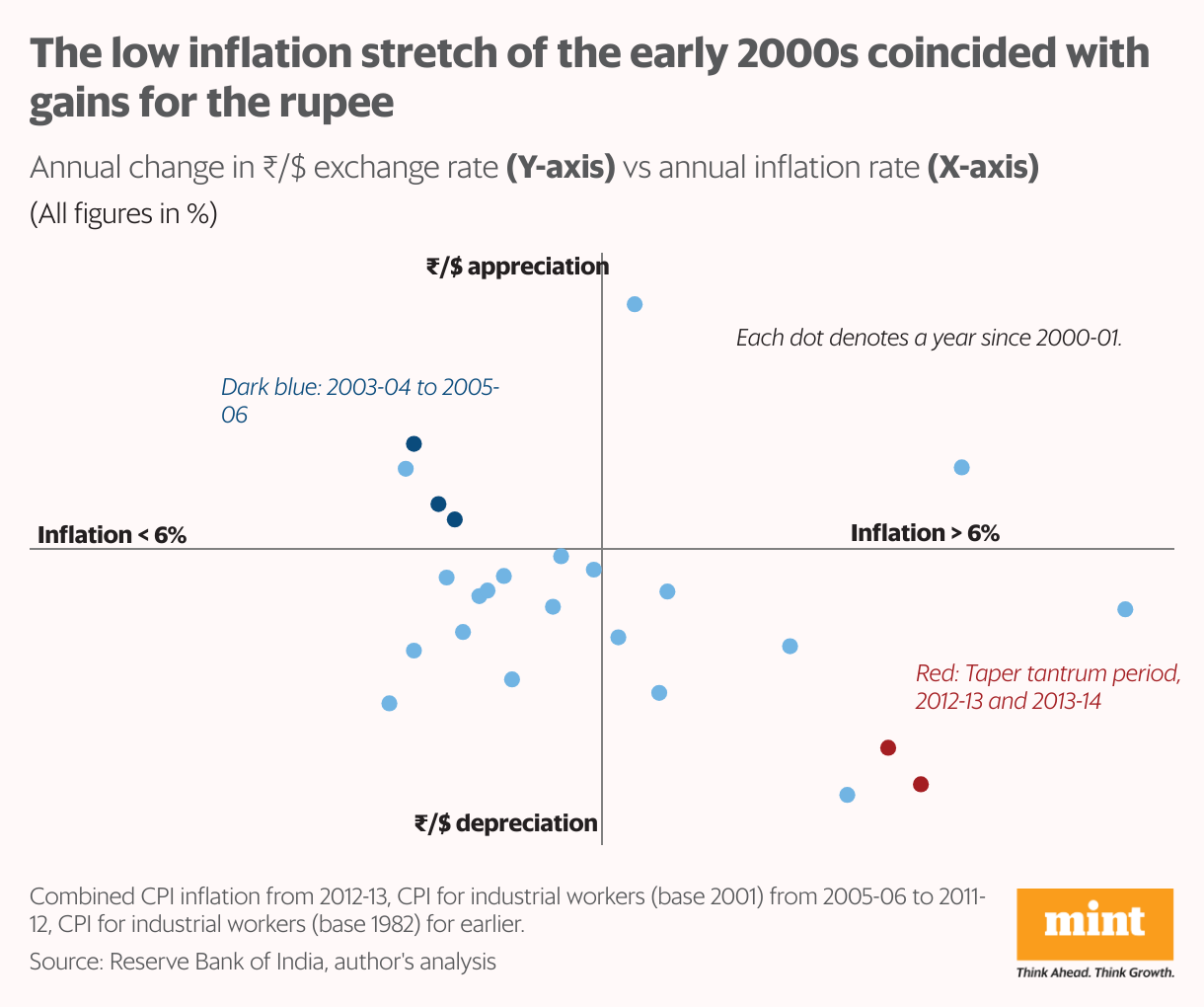

The key impact, as Nageswaran noted in his speech, will be on the rupee’s exchange rate. On a day-to-day basis, the rupee-dollar exchange rate fluctuates in response to actual and expected dollar flows. But in the long run, exchange rate depreciation tends to be related to inflation differences between economies, as per the theory of purchasing power parity.

The inflation differential between the US and India has fallen significantly since the RBI adopted inflation targeting in June 2016. The average gap in the FIT era is about 1.6%, a big drop from the 6%-plus gaps in the years preceding it.

If India’s inflation remains low and stable, the gap is likely to remain narrow, so the rupee may fall by less than the usual 1-3% annual depreciation rate.

In fact, barring short-term market disruptions, the rupee may even see some appreciation. That’s not just wishful thinking: between 2003 and 2006, a period of relatively benign inflation and strong growth resulted in the longest period of gains for the rupee in India’s post-1991 history.

Volatility check

Low inflation may be the end goal, but for policymakers, controlling volatility in prices is equally critical. When inflation is predictable (and preferably, low), it is easier for households and businesses to plan current and future spending.

A review of the FIT framework in an August 2025 RBI discussion paper shows that not only has the level of headline inflation declined since 2016, but it has also become less volatile.

Going forward, if this volatility stays low, policymaking could be transformed in several ways:

- First, interest rates would need to be hiked less frequently to manage inflation. Each instance of policy tightening dampens growth, so fewer such episodes would result in more stable growth.

- Second, RBI would be able to look through occasional inflation spikes, with the confidence that temporary price bursts will neither persist, nor be transmitted to core inflation. A central bank that is not constantly fighting inflation can shift focus, when necessary, to other priorities such as growth or financial market stability.

- Third, the ability to stay on or below the inflation target makes it possible to run the economy on low interest rates. Lower rates stimulate consumption and investment. The resulting pick-up in demand could boost corporate earnings, while lower discount rates would improve share valuations.

All this also makes fiscal expansion possible on two fronts: stable growth ensures steadier tax collections, which, in turn, improves government finances. And lower interest rates keep the cost of servicing government debt down.

Already, declining inflation and consistent fiscal discipline have opened up policy space for fiscal and monetary easing. Since the start of 2025, the government has cut income tax and rationalized indirect tax rates, and RBI has eased interest rates and reduced the cash reserve ratio.

Domestic and China factors

The hope is that the stimulus will make up for growth headwinds from external uncertainties. But the question is—can this growth push be sustained, or will another wave of rising inflation push the economy back into a tightening cycle? The answer depends on how various domestic and external factors play out.

On the domestic front, GST rate rationalization is likely to hold down prices of daily items. Crude oil prices are expected to decline due to rising global inventories, as per the US Energy Information Administration.

In its October monetary policy, the RBI has predicted benign food prices on the back of a reasonably good kharif harvest and ample food grain buffers.

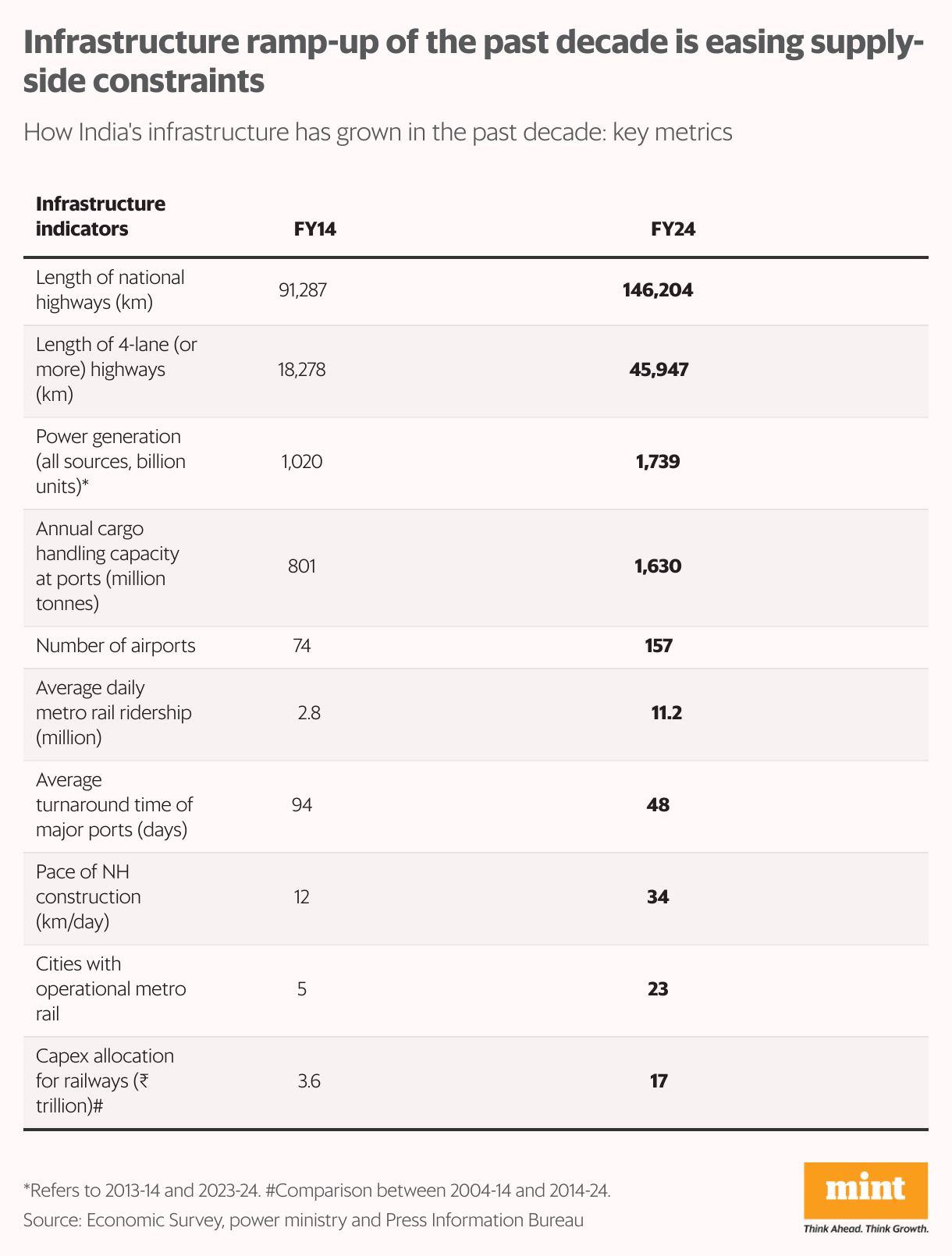

India has invested heavily in physical infrastructure over the last decade. Improvements in roads, railways, airports, shipping, power, water, and rural development are expected to ease transportation bottlenecks. The reduction in supply chain frictions and logistics costs is also likely to put downward pressure on prices.

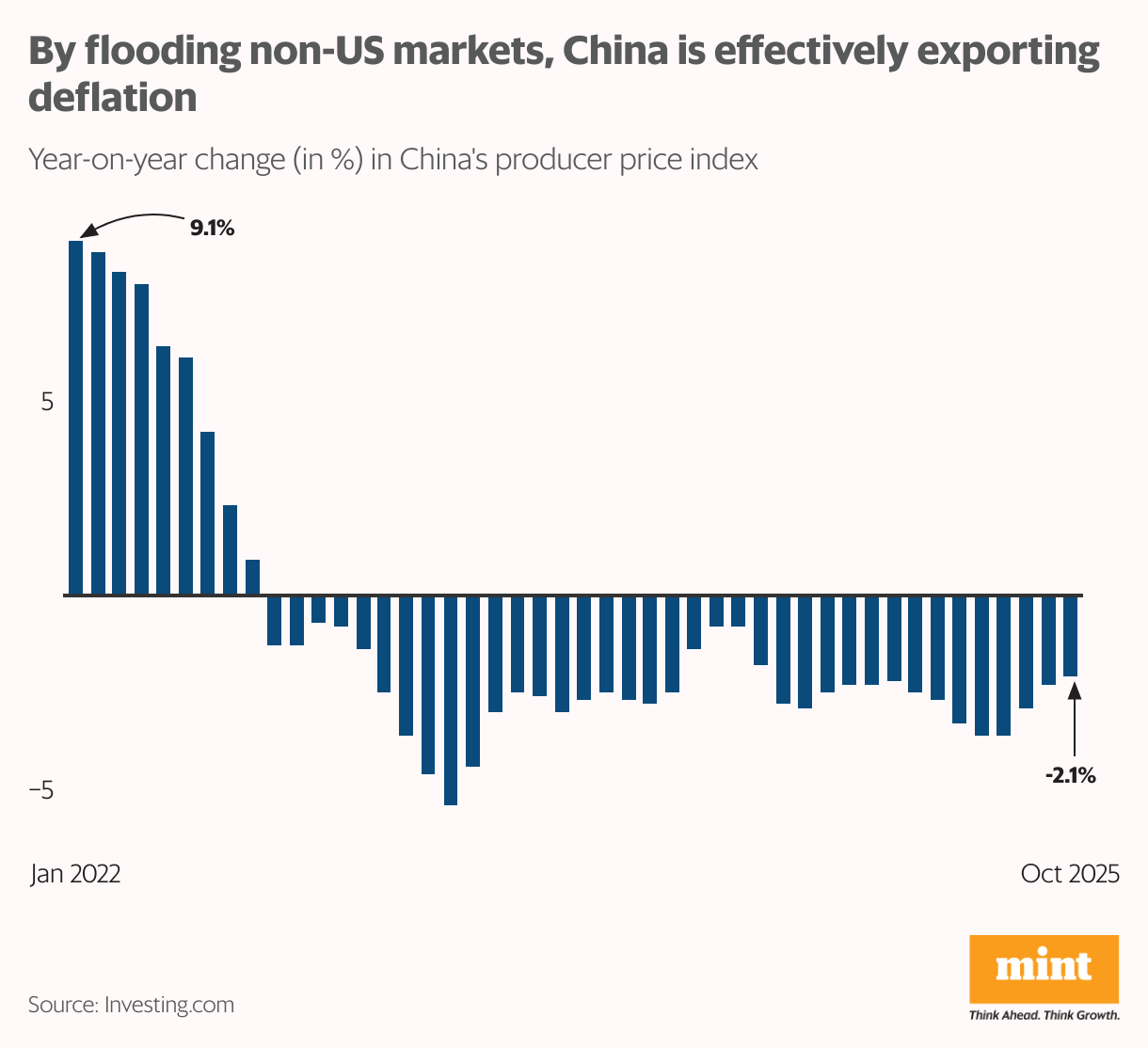

On the external front, China is facing deflation, mainly due to huge overcapacities and low domestic demand. As the US puts up tariff barriers, Chinese exports have flooded other markets at cheap prices; thus effectively exporting deflation to other economies. This situation may continue until US-China trade is restored or Chinese domestic consumption picks up.

Two decades after the 2003-2007 boom, India could once again be on the cusp of a growth cycle, this time driven by a structural downward shift in inflation. The previous boom was halted by the global financial crisis and a series of policy mis-steps. Hopefully, this time round, no opportunity to grow will be squandered.

The author is an independent writer in economics and finance.