As finance minister Nirmala Sitharaman sets out to present her record ninth consecutive Union budget, the Indian economy is experiencing a rare goldilocks period of high economic growth and low inflation. At the same time, uncertainty abounds as the world is disrupted by geopolitical crises and tariff wars which have upended global trade like never before. This will engage the FM’s attention. She is also well aware that India’s enviable headline numbers mask some inherent challenges. The economic expansion, for instance, is powered largely by government spending, with other engines of growth such as private investment, public consumption and exports remaining sluggish. To sustain a high rate of growth, all of them have to contribute strongly and the budget is expected to provide the necessary impetus for that. The need for reforms has never been felt more urgently. The government has already initiated some significant reforms, but a lot more needs to be done. The budget will be the right platform to set out the reform vision for 2026-27 and beyond. Mint has identified eight elements that one should watch for in this budget. They will determine the growth trajectory of the Indian economy.

The Good and the Bad

The good news is that India continues to be the fastest-growing large economy in the world. The first advance estimates from the government pegs 2025-26 real gross domestic product (GDP) growth at 7.4%. To improve the quality of data, India will adopt a new base year of 2022-23, replacing the earlier base of 2011-12. The new series will better reflect the structural changes in the economy. But it remains to be seen how growth numbers will pan out once it is implemented next month. However, what should be more worrying to the policymakers is the low nominal growth rate (which does not even out inflation). At 8%, it is lower than 10.1% assumed for 2025-26 in the budget. This would mean a shortfall in revenue mobilization. How bad will this be, and will the government cut back spending to meet its fiscal deficit target?

Run a tight ship

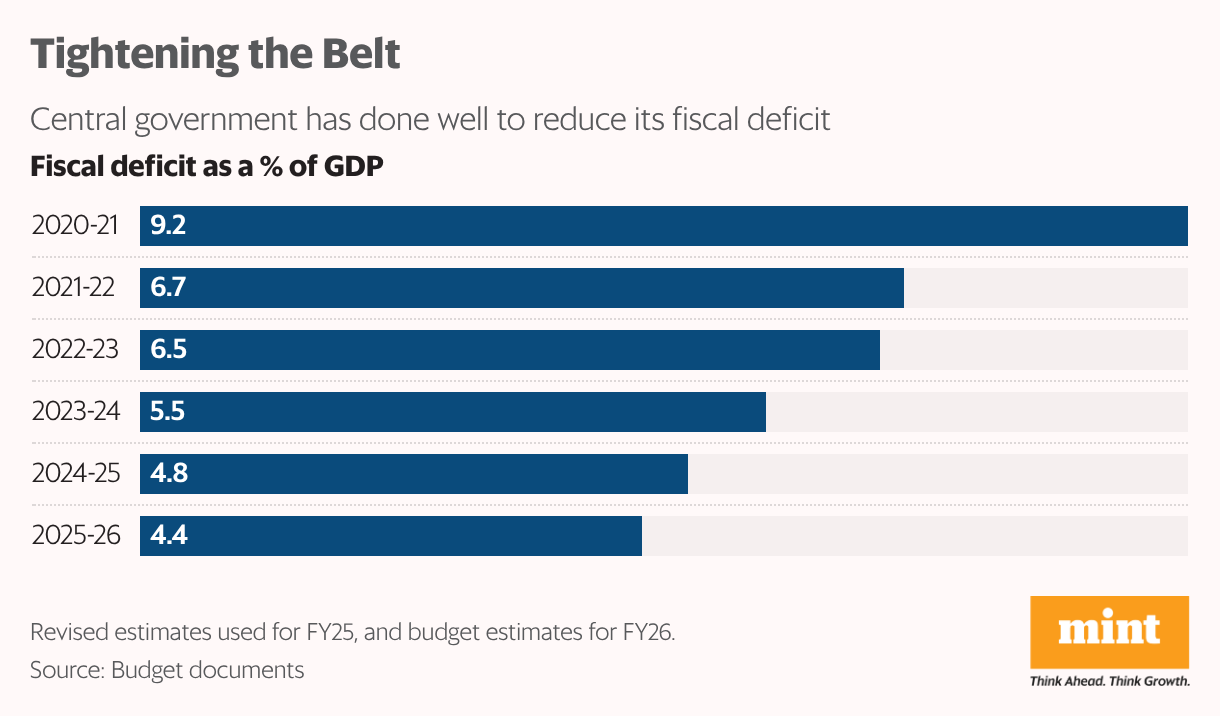

Despite lower tax revenues, the government is expected to meet its fiscal deficit target of 4.4% this year with help of higher non-tax revenues (read higher dividend from the Reserve bank of India) and some expense trimming. The government has done well to focus on fiscal consolidation. It has reduced the fiscal deficit from a high of 9.2% of GDP post-pandemic in 2020-21 – a bit too late, considering that the Fiscal Responsibility and Budget management Act 2003 targeted a fiscal deficit of 3% of GDP by March 2008. The government has announced that from next year, debt as a share of GDP, and not fiscal deficit will act as a measure of fiscal consolidation. It has announced that by 2030-31, its debt as a share of GDP will be brought below 50%. Will the government provide, as markets expect, a year-wise glide path for debt reduction?

High on debt

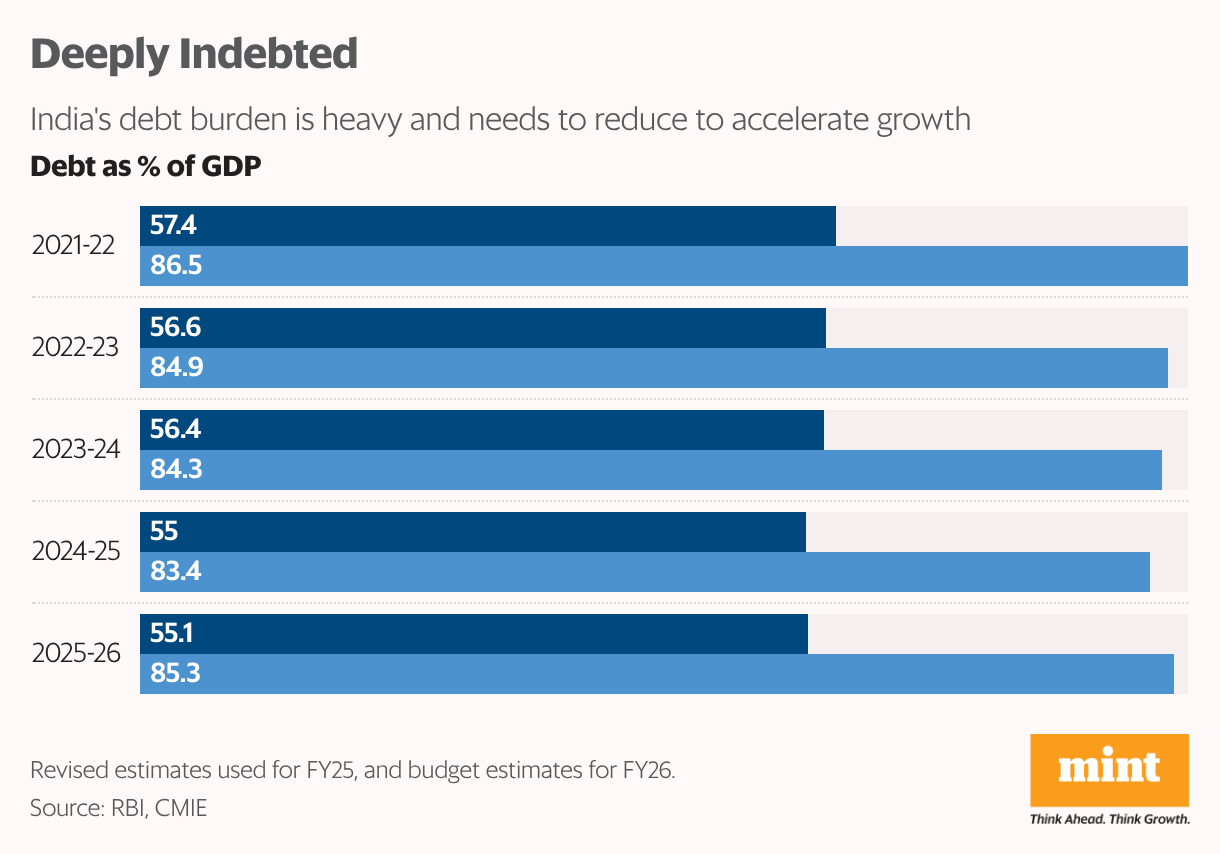

Reducing fiscal deficit, and thereby borrowings, is critical for an emerging economy like India. High deficit increases borrowings. High government borrowings crowd out the private sector from the debt market and push up interest costs. That explains why the Indian industry pays at least 400 basis points more as cost of debt compared to their competitors in other economies. The Centre’s debt in 2025-26 is pegged at 55% of GDP, and if borrowing by states are factored in, this figure bloats to 85.23%. While the Centre has announced a road map to reduce its debt, the states are in no position to do it. In fact, they are under pressure to borrow more as their spending, including on populist policies, has risen even as their revenues declined. Without lower interest rates, the domestic industry will not become competitive in this turbulent external market. Can FM do anything to rein in government borrowing?

Missing animal spirits

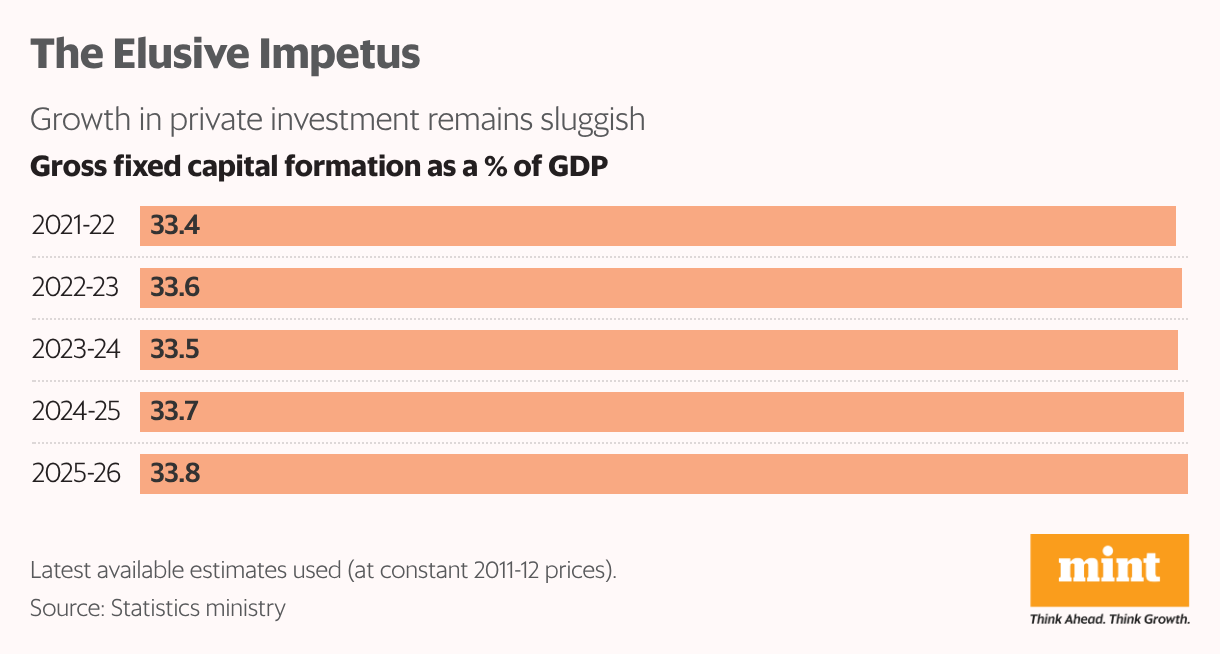

Apart from high interest rates, inadequate demand and lower capacity utilization are seen as reasons for low private investment, despite significant efforts by the government. It has cut corporate tax and spent heavily on infrastructure, in the hope that it will pump-prime private investment. Gross fixed capital formation (GFCF), a proxy indicator for investment in the economy, has not seen any significant improvement in recent years. In 2007-08, when the Indian economy last experienced an unleashing of animal spirits, GFCF touched an historic high of 35.8% of GDP. That was a time when strong government spending on infrastructure was complemented by strong industrial expansion. The government has recently cut tax rates to catalyze demand and announced deregulation to improve the ease of doing business. What more can the FM do to get the private sector to shed their inhibition and start investing?

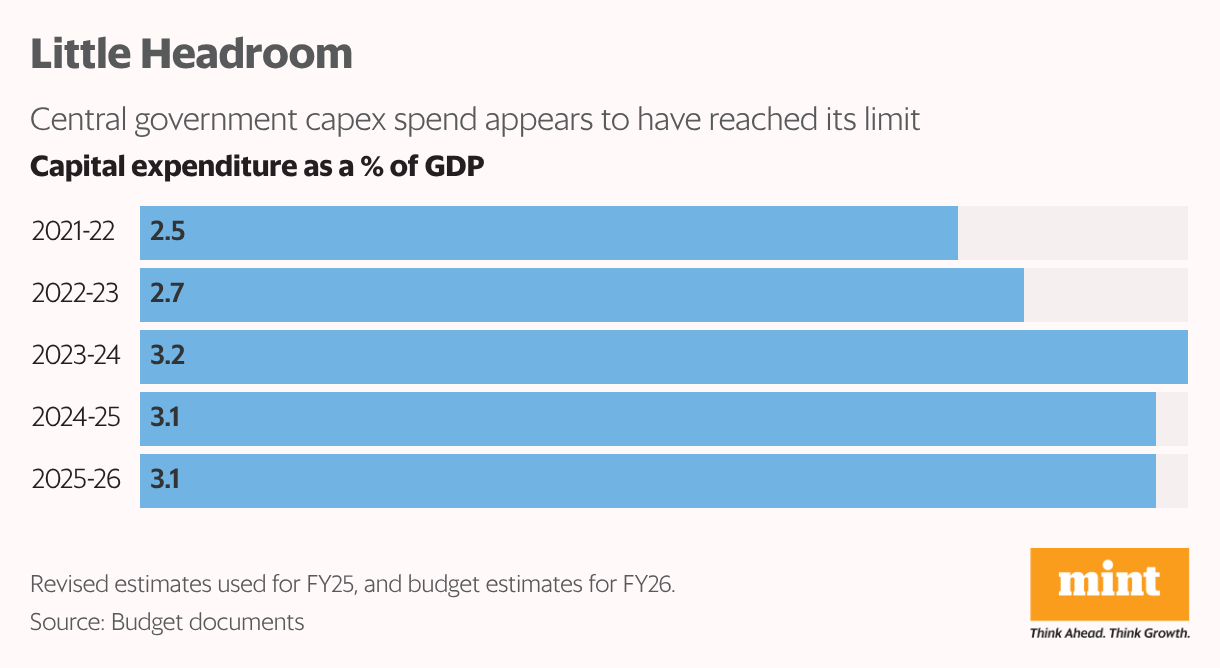

Limited scope

The government’s keenness to revive private investment is understandable. It has been powering economic growth through its spending on infrastructure. Between 2021-22 and 2025-26, the share of capex as a percentage of GDP has risen from 2.5% to 3.1%. It has also got the states to invest in infrastructure by offering them 50-year interest-free loans. This effort appears to have reached its limits for two reasons. One, the government’s ability to spend heavily on infrastructure is being curtained by its fiscal responsibility commitments. That explains why the share of capital expenditure is plateauing at 3.1% of GDP. Secondly, the ability of the economy to absorb the budget capital expenditure is also in question. In the last few years, the budget amount was not spent fully. In 2024-25, the shortfall in spending versus the budget value was 9%. Will FM still enhance capex spending this time? If so, to what extent?

A taxing headache

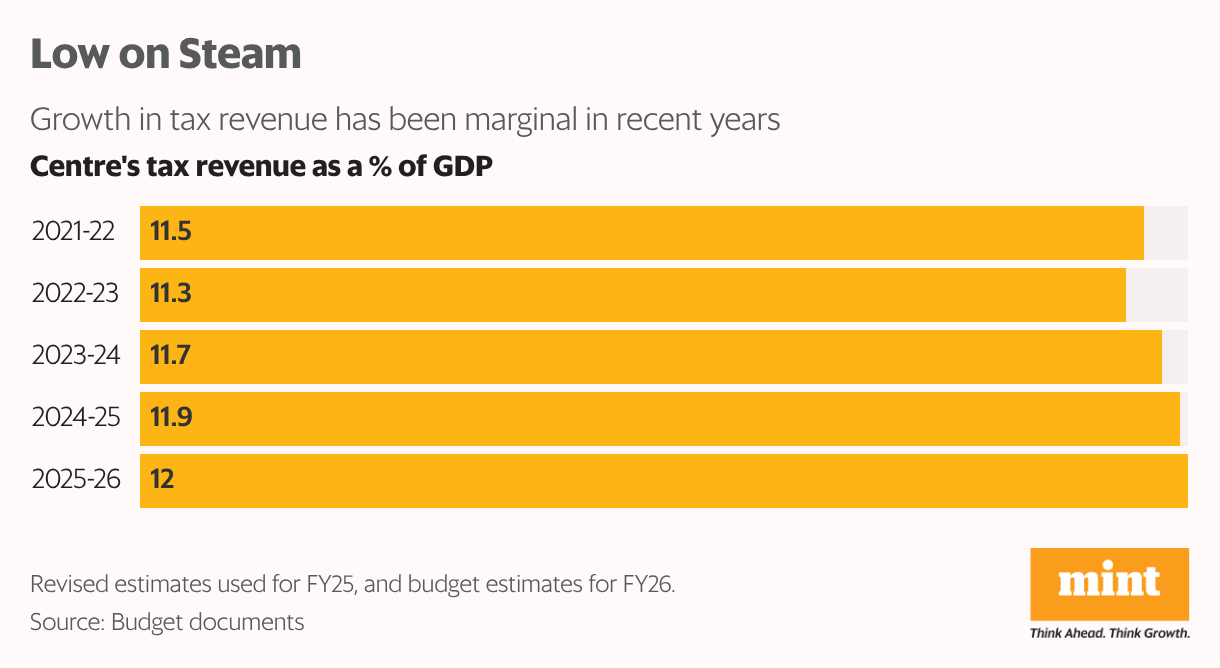

In a rapidly growing economy, revenue mobilization should be the last thing a government should worry about. But that has not been the case, as the government over the years struggled to increase the share of taxes as a share of GDP. Between 2021-22 and 2024-25, the share of taxes as a percentage of GDP has risen from 11.5% to 11.9%. This year, a 12% share has been budgeted, but it is most likely to fall short. According to CareEdge Ratings, tax revenues are estimated to miss their target by at least ₹3 trillion in 2025-26. Sharp cuts in GST rates and income tax benefits have contributed to this situation. As a result, the government has leaned on non-tax revenues such as higher dividends from the RBI and public sector units to save the day. Will the FM come up with ingenious means to increase the tax base and improve tax collections?

Missed opportunity

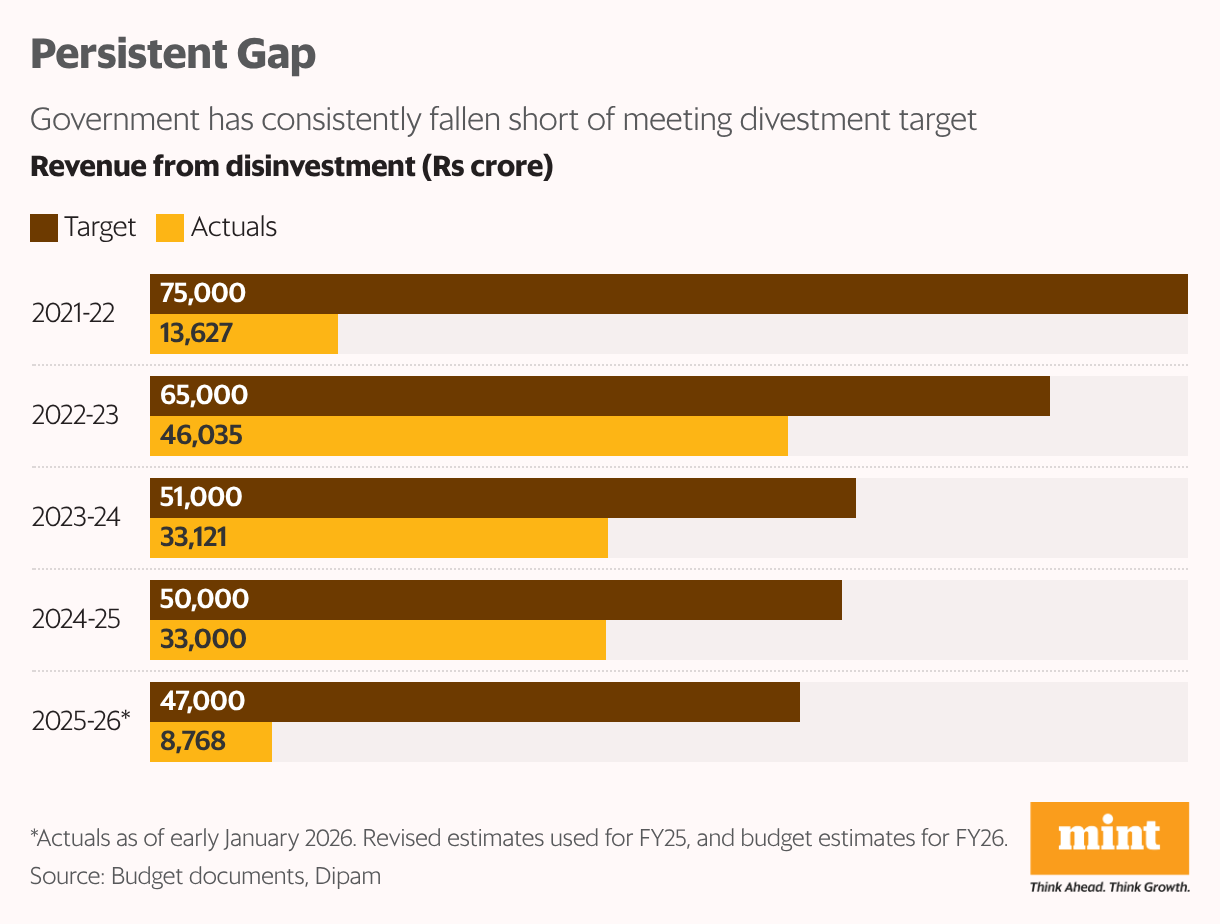

Though the government’s reliance on non-tax revenues has been high in recent years, one non-tax levy it has chosen to ignore consistently is divestment. The chart clearly shows that a huge gap exists between its intention and execution year after year. This year too, the latest numbers show that the government will fall short. Of the ₹47,000 crore it has budgeted, it has raised just ₹8,768 crore till early January. It was betting big on the divestment of its 30% holding in IDBI Bank. It could have yielded about ₹36,000 crore. But the sale is unlikely to go through this fiscal year due to procedural delays. The government had announced that it will focus on asset sales to bolster its non-tax revenues but that has not happened so far. Will the shrinking revenues force the FM to take disinvestment more seriously?

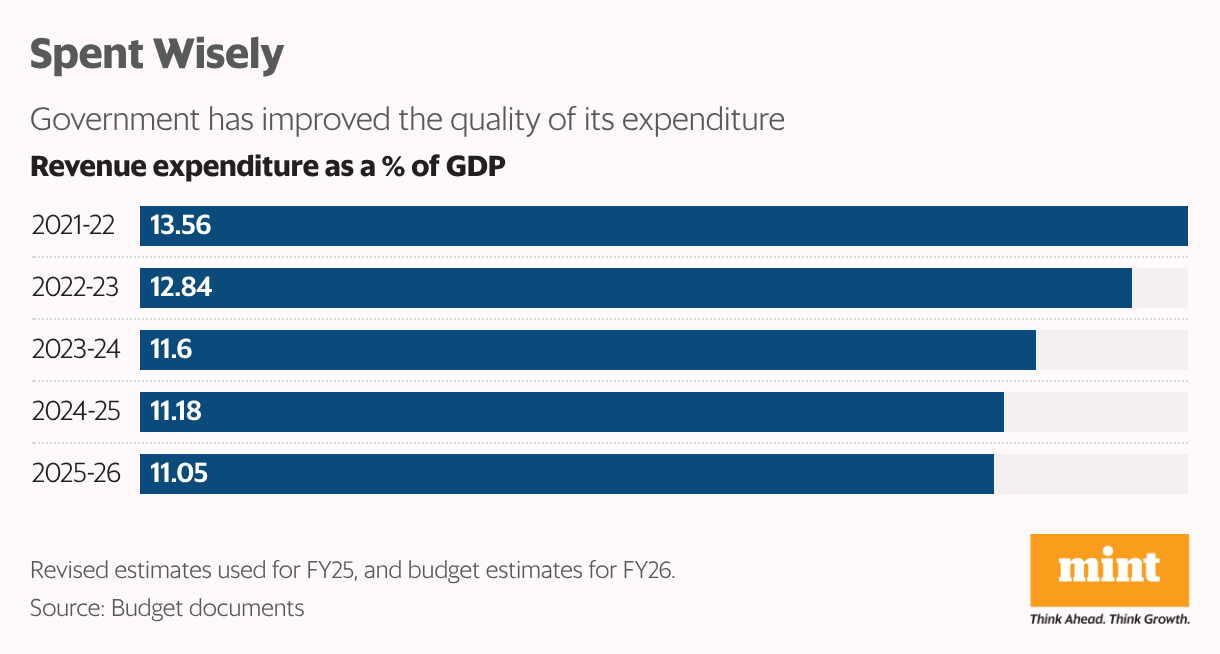

Quality spending

The central government has spent wisely over the years. It has cut back unnecessary revenue expenditure and enhanced capital expenditure. The share of total revenue expenses as a share of GDP has declined from 13.6% of GDP in 2021-22 to 11.1% in 2025-26. The funds it spent on capex has risen from ₹5.9 trillion in 2021-22 to ₹11.2 trillion budgeted for in 2025-26. By focusing on capex, the force multiplier in the economy has been enhanced, say experts. It is time for the states to adopt a similar approach. Though they are increasing their capital expenditure, thanks to interest-free 50-year loans, not enough steps have been taken to reduce unnecessary revenue expenses. This causes them to borrow more. Will the FM incentivize the states to improve the quality of their spending?